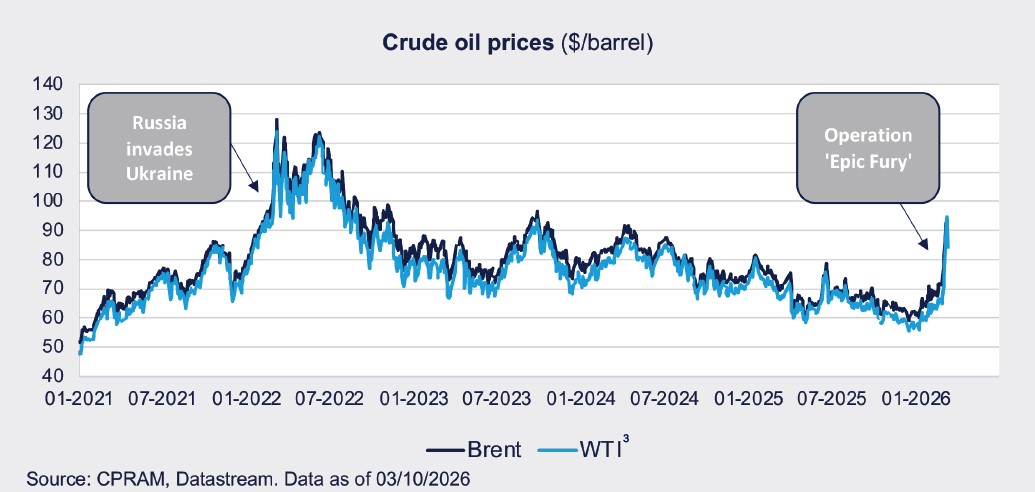

Energy markets shaken by the operation "Epic Fury"

The United States and Israel launched Operation Epic Fury on February 28, in which airstrikes targeted Iranian regime infrastructure and figures, including Ayatollah Khamenei. Iran's retaliation has led to a sharp drop in maritime traffic at the Strait of Hormuz, which has propelled oil and gas prices. Here we come back to the essential points for the energy market.

Published on 13 March 2026

What does Iranian oil production represent?

The 1970s were marked by two oil shocks (1973/1974 and 1979/1980), which caused a long phase of high inflation. The second oil crisis had its epicenter in Iran with the Islamic Revolution of 1979. At the time, Iran was the fourth largest oil producer in the world with a peak of 6 million barrels/day, or about 10% of world production, and about 90% of Iranian production was destined for export1. Iranian production collapsed following the Revolution and has never recovered.

Nowadays, it is estimated that Iran produces between 3 and 3.5 million barrels/day, or about 3% of world production, and about half of Iran's production is destined for export. Since 2019, the United States has put in place sanctions against entities that would buy Iranian oil and it is generally estimated that China accounts for more than three-quarters of Iranian oil purchases1.

Iran's weight on the oil market is therefore much less important than in the 1970s. In addition, the US strikes of June 2025 (Operation "Midnight Hammer") showed that the US was not targeting Iran's oil and gas infrastructure. As part of Operation Epic Fury , the United States has so far not targeted oil and gas infrastructure in Iran and Israel has targeted oil storage sites, which seems to have been disliked by the Trump administration according to press reports.

Why is the Strait of Hormuz so central?

Iran's retaliation and threats of attacks on cargo ships following the launch of Operation Epic Fury by Israel and the United States have led to a sharp drop in maritime traffic in the Strait of Hormuz. The significant increase in insurance premiums has prompted several freight companies to refrain from crossing the strait. This de facto closure of the strait has had particularly significant consequences on energy markets as around 20% of the world's oil and LNG2 exports pass through this strait.

This very quickly hurt crude oil production because the Gulf countries did not have enough storage capacity. Iraq, which had the lowest storage capacity, has already had to reduce its production by about 3 million barrels per day. Other countries could follow if the conflict continues. Estimates on March 10 showed a drop in crude oil production ranging from 6 to 7 million barrels/ day. This represents a definitive drop in production and that is why prices have risen sharply. During the session, Brent crude, for example, exceeded $100 a barrel on March 9.

Developed countries have mentioned putting 300 to 400 million barrels of oil held in strategic reserves on the market, which would represent 25 to 30% of them and make it possible to compensate for 15 to 20 days of total halt in maritime traffic in the Strait of Hormuz.

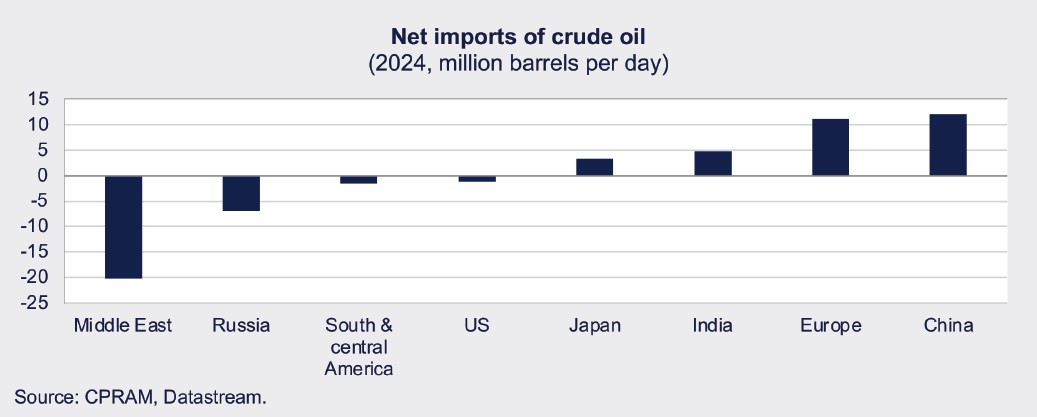

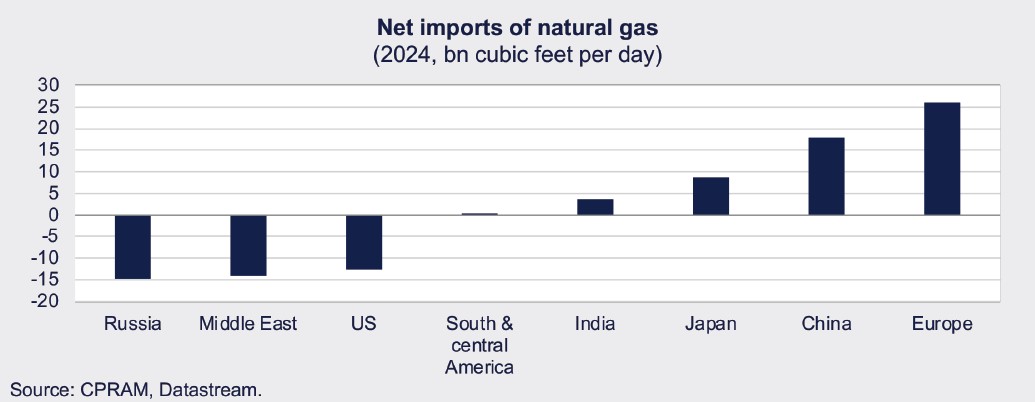

Which countries are most affected by rising prices?

- Asia and Europe are two major oil and gas importers and would therefore be strongly impacted by a sharp rise in the price of oil and gas.

- On the other hand, Russia and the Middle East are very exporters.

- After decades of significant imports, the United States has become an exporter of oil and especially natural gas. This is one of the reasons why gas prices in the United States have remained almost unchanged since the beginning of the conflict.

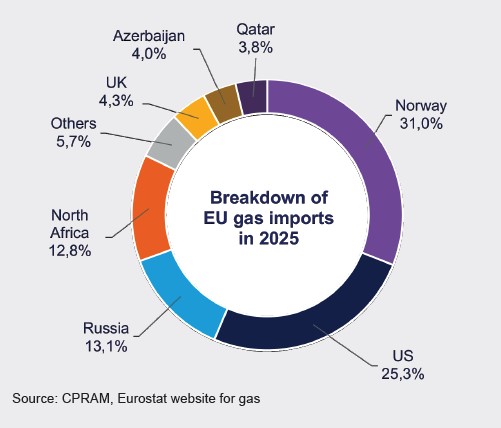

For Europe, a risk of gas supply?

For Europe, the situation with regard to natural gas supply is very different from that of 2022, when Russia accounted for around 40% of the European Union's gas imports. In 2025, Norway was the EU's largest gas supplier (31%), followed by the United States (25%). The main country in the Middle East whose LNG the EU imports is Qatar, which accounted for 3.8% of imports in 2025. Unlike the 2022 energy crisis, the current situation does not seem to put EU gas supplies at risk. It should be remembered that European imports of American LNG have increased very sharply in recent years and are expected to continue to increase if we refer to the US/ Europe trade agreement signed in 2025.

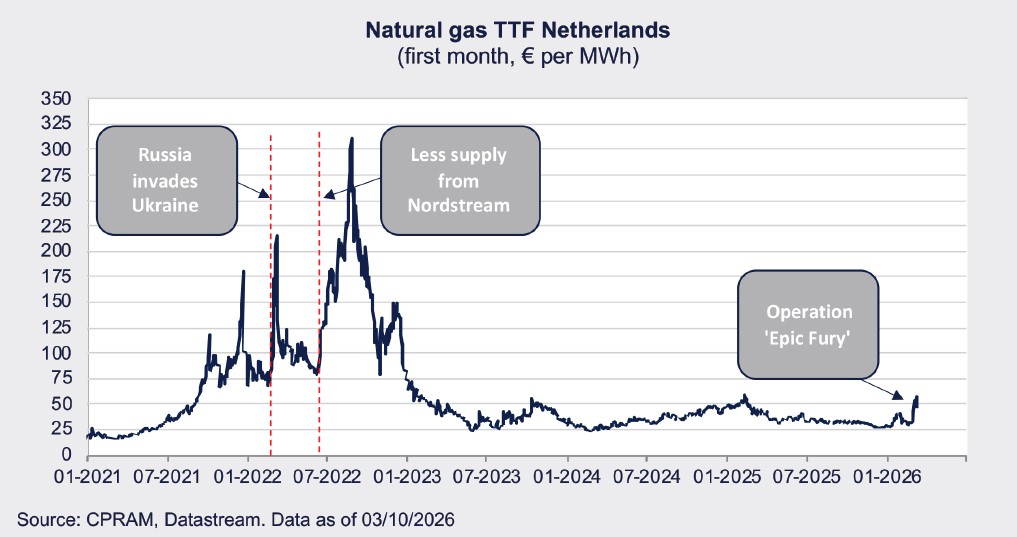

These factors explain why the price of gas on wholesale markets in Europe has risen significantly since the beginning of the conflict, but remains well below the levels reached in 20224.

What would be the impact of a persistently high barrel of oil?

Keeping oil prices high would obviously be negative for activity: for example, a barrel at $100 would represent, to a first approximation, a loss of purchasing power of $25 billion per month for American households, with an unchanged volume of consumption. The negative impact on activity would ultimately have a negative impact on the labour market.

As for the impact on inflation, the impact is more difficult to determine. Of course, a 50% increase in the price of oil (i.e. what the rise of WTI from $67 to $100 represents) would imply a direct increase in headline inflation of about 1.5 percentage points. But deteriorating economic conditions would result in a decline in core inflation, as suggested by the Fed's macroeconomic simulation models, leading the Fed to a dilemma: should we focus on headline inflation or core inflation? The same goes for the ECB, even though the ECB's chief economist, Philip Lane, indicated in the early days of the conflict that the context in Europe was such that there was no risk to be taken with inflation.

For the Fed, the situation would be different from the rise in energy prices in 2022 since the US labour market was historically tight at the time (2 open positions per unemployed person at the beginning of 2022) while this is much less the case now (0.9 open positions per unemployed person). The context would therefore be much less conducive to the development of secondround effects and even the most hawkish5 members of the FOMC6 would not necessarily be inclined to call for key rate hikes. On the contrary, there is no doubt that Kevin Warsh, if confirmed by the Senate, would be even more eager to obtain rate cuts.

What are the longer-term impacts?

The market impacts, which are generally negative for risky assets outside the energy sector, will obviously depend on the duration of the conflict and its possible spread. However, several assumptions can be made about the long-term impact:

- Geopolitical tensions, already at their highest level in decades, continue to rise. Overall military budgets could continue to increase sharply and over time. (cf the 50% increase in the defense budget requested by Trump in Congress in January)

- Coupled with trade tensions, the rise in geopolitical tensions could ultimately favour precious metals (especially in a context that favours a little more the increase in public debt, via the deterioration in economic activity).

- The even more tense energy context could intensify global competition for the security of critical materials.

.1. Source: Datastream.

2. Liquefied Natural Gas.

3. WTI: West Texas Intermediate (benchmark crude oil in the USA)

4. Source: Eurostat website for gas

5. Hawk: members of the central bank in favor of a more restrictive monetary policy, who are the strictest on inflation and favor high interest rates and a

restrictive monetary policy.

6. FOMC: Federal Open Market Committee.