Assessing the Powell years: An ordinary presidency in extraordinary times

Kevin Warsh is expected to take over as Fed Chair in the coming days, marking the end of Jerome Powell’s eight-year tenure on May 15. This is an opportune moment to step back and review Powell’s presidency.

Published on 5 May 2026

A tenure marked by a succession of shocks

It is unreasonable to judge a central banker’s presidency without considering the context he faced. Unlike the calm four years under Janet Yellen (2014–2018), Powell’s years were marked by a series of crises of very different kinds.

The U.S. economy faced four major supply shocks during Powell’s presidency:

- The COVID pandemic in 2020,

- Russia’s invasion of Ukraine in 2022 and the resulting energy crisis,

- The trade war initiated by Donald Trump upon his return to the White House in 2025,

- The war in Iran in 2026 and the sharp rise in fuel prices that followed.

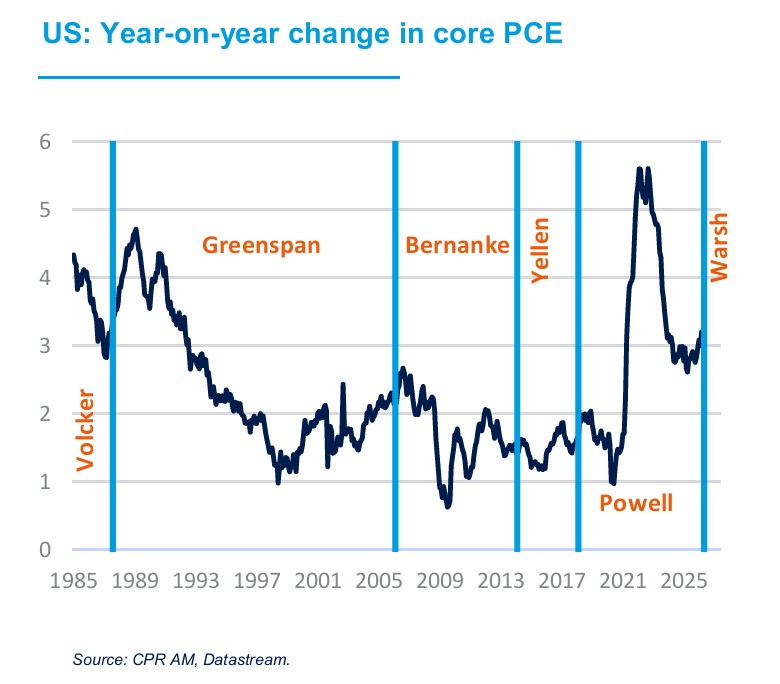

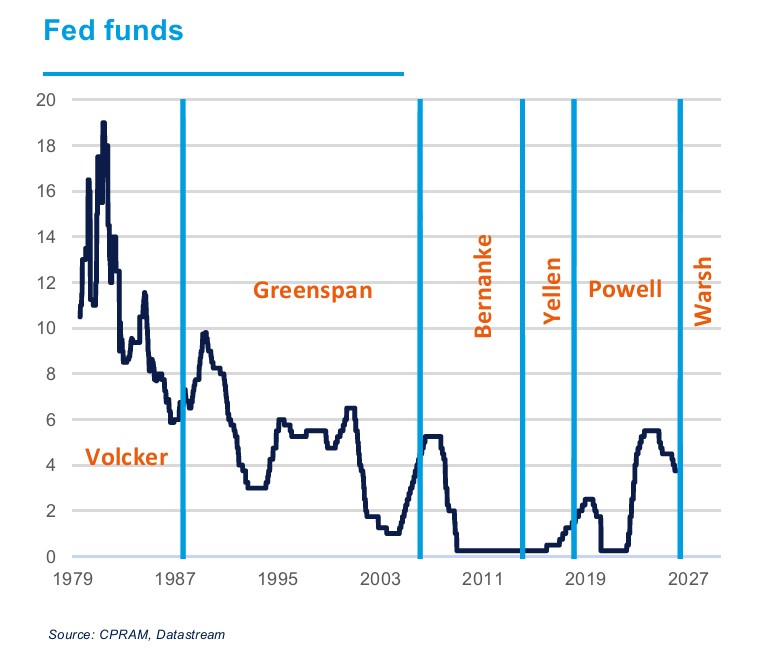

Supply shocks are always difficult for central banks to manage, as they can lead to simultaneous increases in inflation and unemployment. For the Fed, this puts tension on its dual mandate (price stability and full employment) and opens the door to a wide range of interpretations depending on individual convictions and preferences. However, the unique context of 2022 and 2023, with very high inflation and an exceptionally tight labor market, left little doubt about the need for vigorous action and sharp rate hikes. By raising the fed funds target range from 0%/0.25% to 5.25%/5.50% in just over a year, the Fed carried out its most aggressive tightening cycle since the Volcker shock of the early 1980s. Powell has never hidden his admiration for Paul Volcker’s determination at the time.

The sharp rise in rates in 2022/2023 contributed to the banking crisis of 2023, during which several commercial banks, including SVB, failed. The swift and forceful response by the Fed, the Treasury, and other federal agencies prevented contagion that could have severely damaged the U.S. economy.

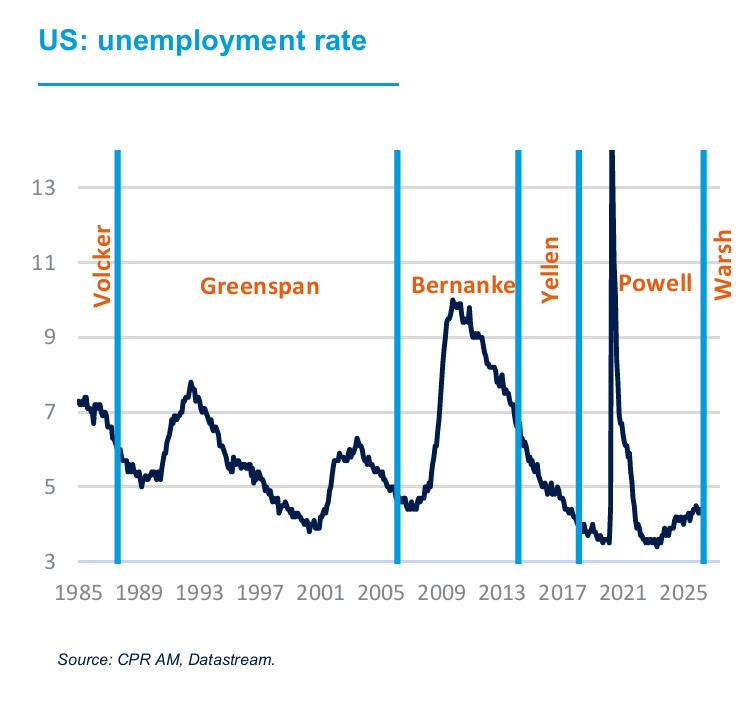

Ultimately, Powell’s presidency was marked by truly exceptional economic events: U.S. unemployment reached both its lowest and highest levels in 70 years, and inflation saw swings not experienced since Volcker’s era. The fact that the U.S. only experienced a two-month recession (February and March 2020) during this period is a credit to Powell.

A presidency marked by nearly two monetary cycles

When Powell took office, the Fed was in the midst of a rate hike cycle, which continued until December 2018, with the fed funds rate peaking at 2.25%–2.50%. The Fed then shifted to rate cuts in the summer of 2019, mainly due to Trump’s first trade war weighing on economic prospects and the stock market—sparking talk of a “Powell put,” reminiscent of the “Greenspan put” thirty years earlier. A few months later, in March 2020, fears of economic collapse during the pandemic prompted the Fed to rapidly cut rates to zero.

Another monetary cycle began as inflation accelerated during the post-COVID reopening (2021) and the 2022 energy crisis. The Fed raised rates aggressively, sometimes by 75 bps, bringing the fed funds target to 5.25%/5.50% by summer 2023. Only at the end of 2024 and then late 2025 did the Fed normalize rates back to 3.50%/3.75%. This rate-cutting cycle was slowed by fears of renewed inflation due to tariff hikes.

Thus, Powell’s presidency was marked by almost two full monetary cycles, distinguishing it from his two predecessors: Bernanke’s years (2006–2014) were almost entirely about monetary easing, and Yellen’s (2014–2018) were about very gradual normalization (only 125 bps of hikes). In terms of rate policy, Powell’s tenure resembles Volcker’s and Greenspan’s, with great flexibility and large moves both up and down.

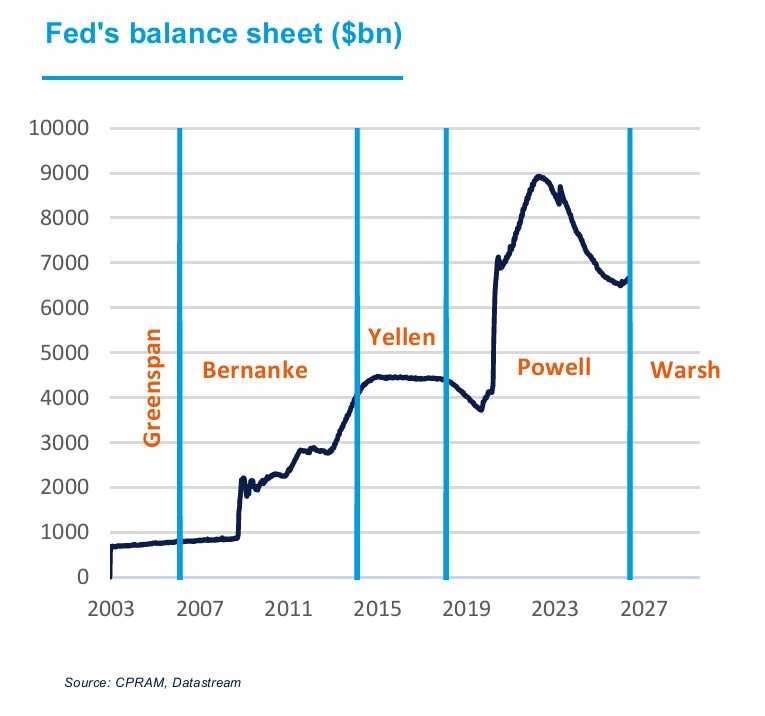

Powell’s presidency also stands apart from Bernanke’s and Yellen’s in terms of balance sheet policy, with deliberate alternation between Quantitative Easing and Quantitative Tightening. In March 2020, the Fed undertook its largest-ever Treasury purchases—$75 billion per day—to “preserve market functioning.” Conversely, from 2023 to 2025, the Fed carried out its most aggressive balance sheet reduction, from about $9 trillion to $6.5 trillion. From late 2025, the Fed resumed “technical QE” to avoid more pronounced tensions in money markets.

Ultimately, whether in rate or balance sheet policy, it is difficult to label Powell as a dove or a hawk, given the flexibility and determination with which both tools were used during his presidency.

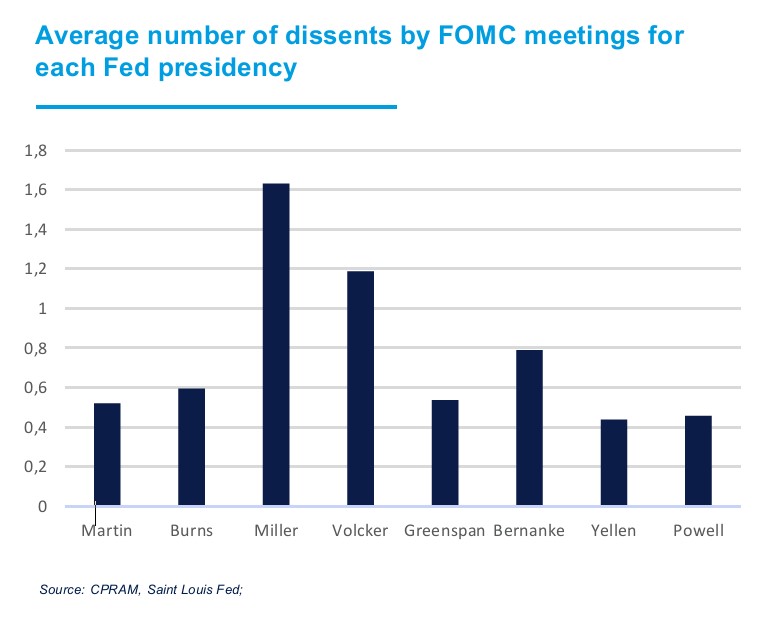

A presidency with very little internal opposition

At Powell’s final FOMC meeting as Chair (April 2026), four members voted against the statement—the strongest opposition since 1992. However, it would be incorrect to assume that Powell’s presidency was marked by strong internal dissent; in fact, quite the opposite is true. Aside from Janet Yellen, no Fed Chair since the 1950s has had so few “dissents” (votes against the FOMC statement).

This low internal opposition is remarkable given the number of supply shocks during Powell’s tenure. As Powell himself noted, these shocks put both inflation and unemployment under pressure, leading to differences in how the dual mandate is interpreted within the FOMC.

A mandate marked by confrontation with Donald Trump

When Donald Trump chose Powell to succeed Janet Yellen in 2018, he likely did not expect Powell to become his chief adversary, subject to frequent insults. Just months into Powell’s term, Trump harshly criticized him for rate hikes.

While U.S. presidents have often criticized the Fed, Trump went further, even asking on Twitter: “Who is our biggest enemy? Jay Powell or President Xi?” Sometimes, Trump’s requests were outlandish, such as demanding negative rates, which the Fed is constitutionally barred from implementing.

Criticism and intimidation intensified during Trump’s second term, as he felt the Fed was not cutting rates quickly enough. In summer 2025, Trump personally inspected Fed renovations, suggesting budget overruns could lead to prosecution. As Powell revealed in a January 2026 video, the Department of Justice opened an investigation, which Powell described as a “pretext” motivated by the Fed’s refusal to set policy according to the president’s preferences. This possible investigation is why Powell did not leave the Fed Board after his term as Chair ended.

The attempt to remove Board member Lisa Cook, brought before the Supreme Court, can also be seen as political pressure linked to Trump’s dissatisfaction with Fed policy. In his final press conference, Powell stated that the Fed’s independence remains at risk.

It is unreasonable to judge a central banker’s tenure without considering the context, and Powell’s years were marked by truly exceptional economic events. The succession of crises led to fluctuations in unemployment and inflation not seen in a generation. Despite this, Powell’s Fed managed the economy well, avoiding recessions except during the strict lockdowns of February and March 2020. This is all the more remarkable given that Powell achieved this with minimal internal division and despite intense pressure from Donald Trump. For his successor, Kevin Warsh, the challenge appears to be extremely daunting, as pressure from Donald Trump is likely to continue and internal divisions could deepen.