A paradigm shift for European defense

While the Trump administration has clearly raised the question of ending US military support for Ukraine, Europe is increasingly aware of the need to establish its strategic autonomy in the military domain. Member states' defense policy has undergone significant changes since 2022 and the start of the war in Ukraine.

Published on 7 April 2025

New projects, notably Rearm Europe and the German budget plan, currently under discussion, should accelerate investment in European defense capabilities. In this context, it is worth taking stock of European defense spending, deployment projects for the coming years, and the financing methods being considered.

The war in Ukraine has radically changed the game

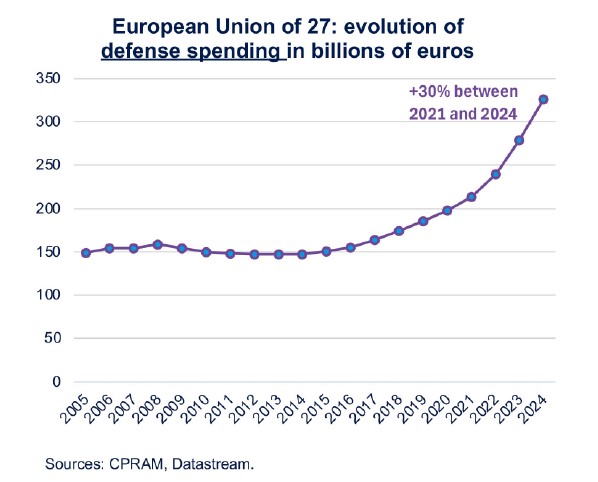

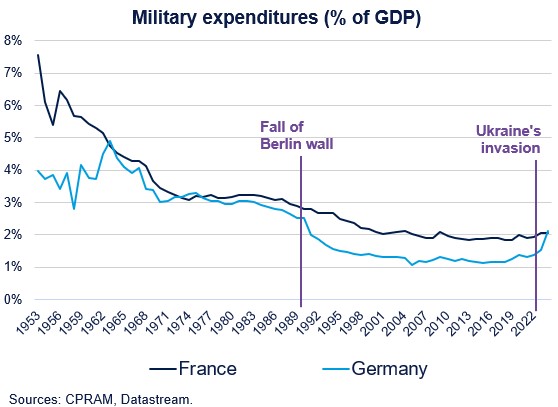

Since the fall of the Berlin Wall, there has been an acceleration in the decline of European military spending, which has decreased from 3% of GDP in 1990 to 1.5% in 2020. The return of war on European territory has altered this trend and caused a rise in military budgets starting in 2022. Thus, between 2021 and 2024, the defense spending of the EU member states increased by more than 30% to reach 326 billion euros in 2024, which is about 1.9% of the EU's GDP. For the 23 EU countries that are also NATO members, defense spending reached 2% of their GDP in 2024 and is expected to rise to 2.04% in 2025.

The war in Ukraine has led the European Union to allocate European funds to Defense. Thus, the multiannual financial framework 2021-2027 allocated 16.4 billion euros for activities related to security and defense. More than 1 billion euros per year have been spent by the EU in this context since 2022. These funds are primarily dedicated to research and development in the defense sector but also to strengthening ammunition production.

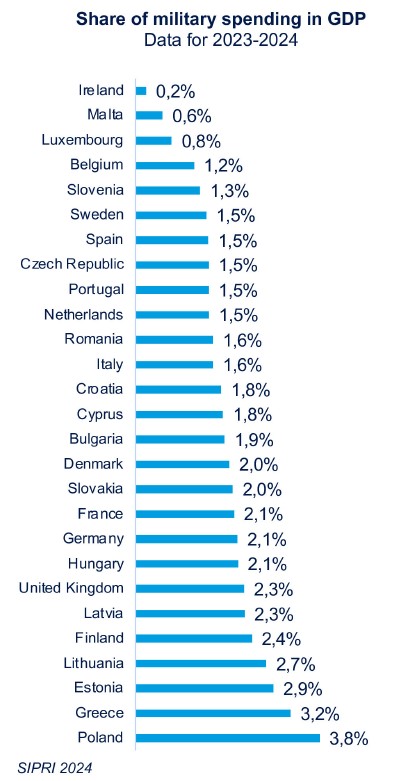

Of course, the data is very heterogeneous within Europe, with significant military budgets in some Eastern countries and levels below the European average for Spain and Italy, but the upward trend is noticeable everywhere.

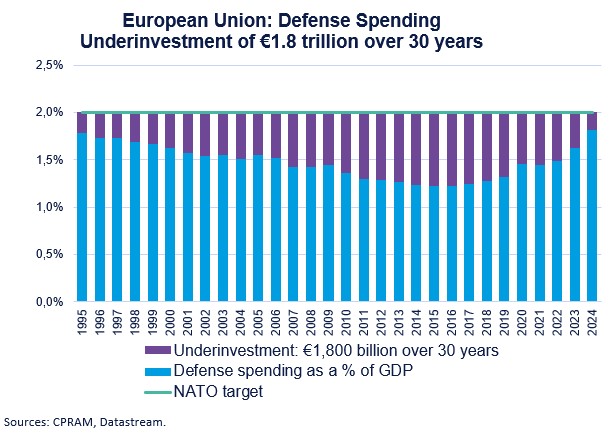

A European under-investment of nearly 2000 billion euros

Over the past 30 years, European military spending has remained well below NATO's target of dedicating 2% of GDP to military expenditures. This has led to a cumulative investment deficit in the defense sector estimated at nearly €2000 billion.

Defense spending: what are we talking about?

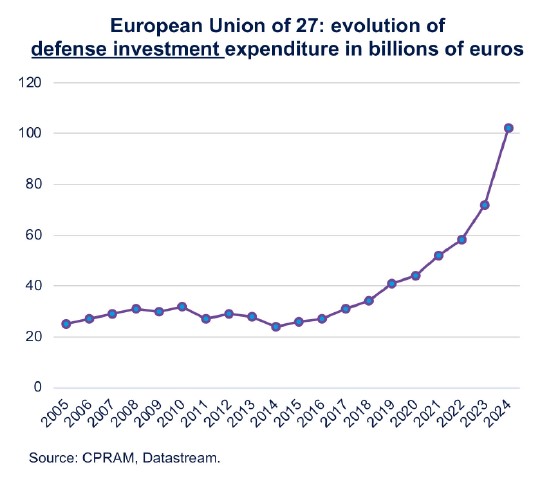

Military spending mainly covers 3 major areas: personnel remuneration, investment (purchases of military equipment: tanks, planes, ships, etc.), and intermediate consumption (purchases of ammunition and consumables). Major military equipment purchases (aircraft, fleet) by the European Union are highly concentrated, as two-thirds of this spending is accounted for by France, Germany, and Italy.

The European Defence Agency has set a target of 20% of defense spending dedicated to investments. It is interesting to note that this target is significantly exceeded in 2024, with nearly 30% of defense spending allocated to investments.

Europe will accelerate its investments in defense

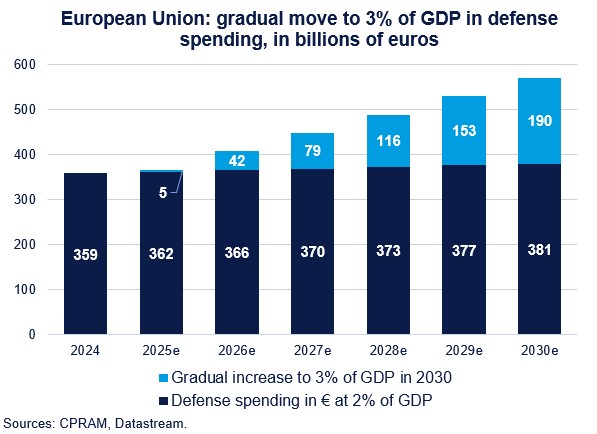

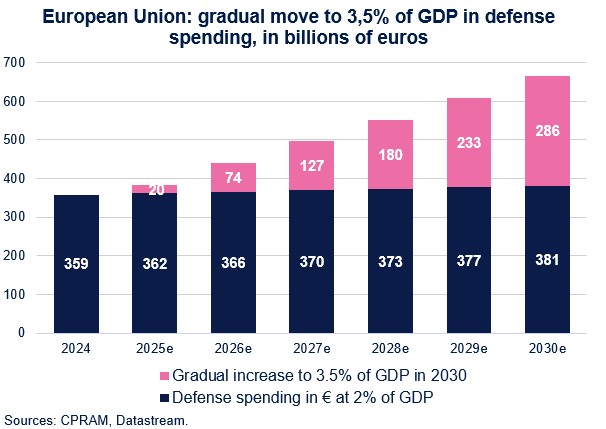

The prospect of American military disengagement in Ukraine constitutes an additional argument for accelerating the increase in military spending. Mark Rutte, the Secretary General of NATO, mentions a new target for military spending of over 3% of GDP, even 3.5% by 2030, while Donald Trump set a target of 5% for Europeans.

The increase in military spending from 2% to 3% of GDP represents nearly €190 billion in additional annual expenditures for European countries. A gradual ramp-up would involve nearly €600 billion in additional defense spending by 2030, and moving to 3.5% of GDP would generate an additional €900 billion in spending.

The question of financing is central for a number of countries that have limited budgetary leeway, or even none for those that are under Excessive Deficit Procedure.

The issue of financing is key

Several avenues are being considered and could be implemented jointly: national public funding, European funding, private funding.

The President of the European Commission proposed a ReArm Europe plan of €800 billion in early March, ahead of a European Council dedicated to defense. She suggests activating several funding levers to increase defense spending beyond the 2% of GDP reached in 2024:

- National funds through the possibility of activating the national derogation clause of the Stability and Growth Pact for defense spending. This would provide budgetary leeway for countries subject to excessive deficit procedures in particular.

- A new European loan instrument, SAFE, for €150 billion for pan-European capabilities, including joint purchases of ammunition. This program is comparable in nature to the SURE program that financed short-time work during the Covid crisis.

- The use of the EU Budget: utilizing programs related to EU cohesion policy to increase defense spending. This is an important point for small countries in particular.

- Mobilizing private capital through the EIB and the savings of European households.

The German Bundestag and Bundesrat have just voted in favor of a very substantial fiscal package that will allow for a significant increase in defense spending. Indeed, it plans to amend the debt brake rule and exempt defense spending beyond 1% of GDP from the limits of the debt brake. The definition of defense spending adopted is broad and includes cybersecurity, intelligence, aid to Ukraine, etc.

Currently, the federal budget allocates €53 billion, or 1.25% of GDP, to defense spending, with the remaining 2.1% of GDP dedicated to defense being covered by an ad-hoc fund endowed with €100 billion, which is set to expire soon.

The European Union and defense

If defense issues fall under national prerogatives, Europe has taken successive initiatives to strengthen cooperation among member states on the subject.

In 2009, the Lisbon Treaty established the creation of the Common Security and Defense Policy (CSDP), which constitutes a framework for cooperation in defense and crisis management. Within this framework, decisions are made by the Council of the European Union by unanimity.

Article 42.7 of the Lisbon Treaty provides for a mutual assistance clause: "If a member state is the object of armed aggression on its territory, the other member states shall provide it with aid and assistance by all means in their power, in accordance with Article 51 of the United Nations Charter. This does not affect the specific nature of the security and defense policy of certain member states."

The European Defense Fund, which aims to support research and development projects among European industries, was established for the budgetary period 2021-2027 with a budget of €8 billion.

Andrius Kubilius was appointed Commissioner for Defense and Space in 2024, thus becoming the first European Commissioner to have a portfolio explicitly including competence on defense issues. His mission includes the objective that states delegate defense competencies to the EU and aims to strengthen the European defense industry.

The European Union's Strategic Compass, adopted for the first time in 2022, defines the main orientations of European defense and security.

Finally, the European Union created the "European Peace Facility," which finances the EU's external military actions and has been notably used to provide military assistance to Ukraine.

What positioning for European defense in the world?

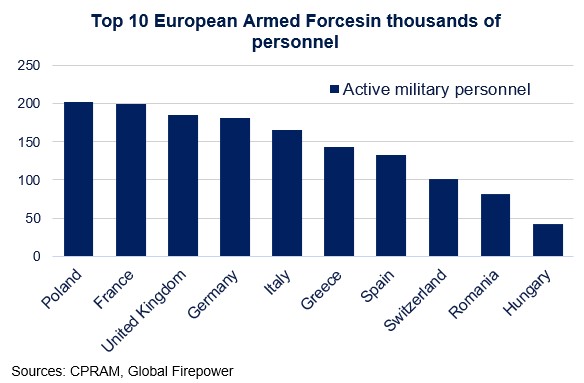

Within the European Union, France has the most powerful army in 2025, according to the Global Firepower website, which establishes a military power index. It ranks 8th, just behind the United Kingdom and Japan. Italy, Germany, and Spain are ranked 10th, 14th, and 17th globally, respectively, while Ukraine is in 20th position.

This ranking incorporates more than 60 criteria related to national defense: possession of nuclear weapons, force projection capability, the ability to conduct external operations…

European military personnel

Starting from the early 2000s, the personnel of European armies has significantly decreased with the professionalization of the armed forces and the end of conscription in most countries in the region. Today, Europe has approximately 1.7 million active military personnel, to which must be added just over 3 million reservists.

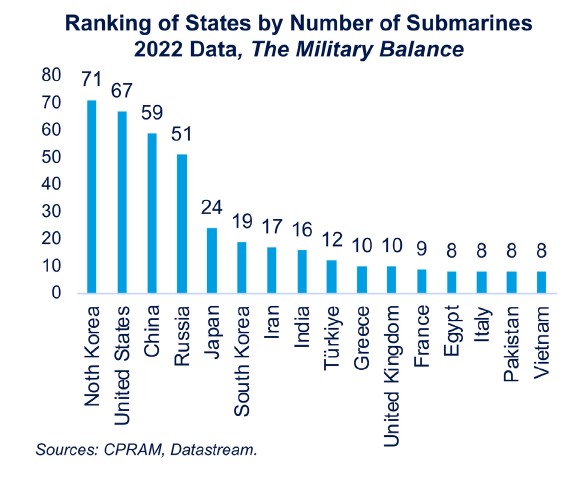

Naval forces

Europe (including the United Kingdom) has naval forces comparable to the two major maritime powers, the United States and China. Indeed, the fleet of European countries comprises about 1900 ships, including around sixty submarines, which is very close to China (1600 ships and 59 submarines) and the United States (1100 ships and 67 submarines).

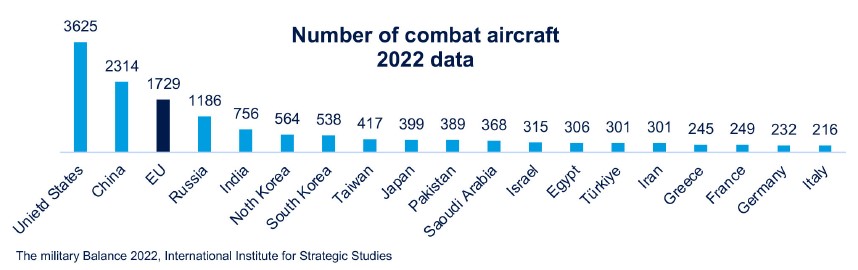

Air forces

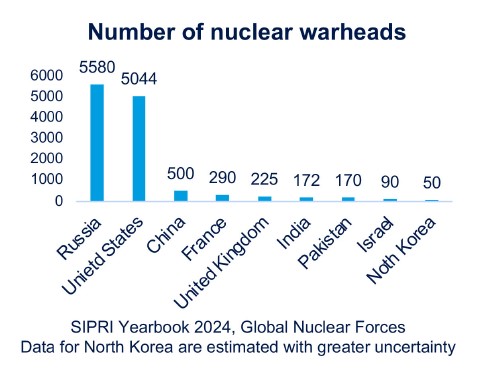

Nuclear power

Two European countries possess nuclear deterrent forces, the United Kingdom and France. Within NATO, several European countries (Germany, Italy, the Netherlands, and Belgium) benefit from nuclear sharing and host American nuclear weapons on their territory.

The European defense industry

The European defense industry is closely linked to the aerospace industry, which carries out both civilian and military missions. It generated a turnover of €158.8 billion in 2023 (+16.9% compared to 2022) and employs 581,000 people. It relies on a broad network of 2,500 SMEs.

In the ranking of the world's leading defense companies published by SIPRI in December 2024, 12 European companies appear in the TOP 50, including 5 French companies.

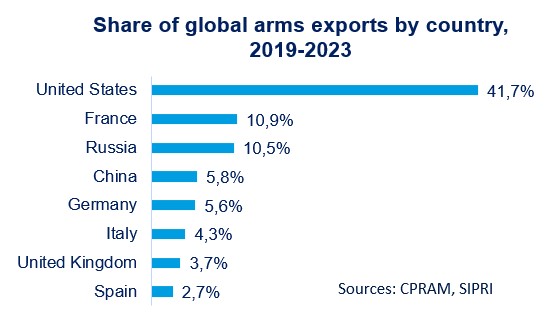

While the United States holds the position of the world's largest arms exporter with a market share exceeding 40%, France has become the second-largest arms exporter (11% of sales) ahead of Russia since the war in Ukraine. The United States and Western Europe account for 72% of global arms exports. European military exports amounted to €57.4 billion in 2023, an increase of 12.6% compared to 2022.

What is the impact of increased military spending on growth?

The budget multiplier, that is to say the ratio between public spending and its impact on activity, is high for investment spending (greater than 1). For military spending, the literature provides very variable conclusions about the level of the multiplier depending on several factors.

First, it is important to see if there is a substitution effect of defense spending compared to other types of public spending. If this is the case, the multiplier is very low or even zero. Next, it is necessary to assess the mode of financing and the nature of the expenditures made. Indeed, it will be important to see if the spending will particularly target personnel, intermediate consumption (ammunition), or investments in equipment.

Finally, it is essential to see to whom the demand is directed: domestic companies or imports. The multiplier is high in the first case and very low in the second.

Moreover, military research and development can have a positive spillover effect on the private sector and thus have a positive effect on growth potential.

These expenditures can take a long time to implement, especially for the defense investment part, and therefore may not have an impact on activity in the short term but rather in the medium term (2-3 years).

Conclusion

Given the current geopolitical tensions, defense is emerging as a central theme of European strategic autonomy. It also aligns with the challenges of reindustrialization and the mastery of cutting-edge technologies by Europe. The recent budget announcements from Germany and Europe place it at the top of public investment priorities. This could have significant impacts on European growth in the coming years, but also on potential growth by allowing for an improvement in European productivity.

Europe without American military support and what goal for increasing military spending?

Europe has defense capabilities that are poorly integrated, and the United States accounts for 50% of its military equipment supplies. Therefore, it currently does not have the capacity to independently ensure its defense. To achieve this goal, it would require military spending well above the ambition of reaching 3% by 2030. It would be necessary to "bridge" the underinvestment accumulated over the past 20 years, estimated at nearly €2000 billion. Military spending should be raised to a range of 3.5% to 4% of GDP for at least 10 years.

Such a level of military spending would face several challenges, including budget constraints and the ability of the European industry to scale up at a sustained pace.

The aim of the increase in military spending in the short term is to strengthen the industrial and technological base of defense and its production capabilities. This is an essential point to absorb the new norm of 3% while reducing exposure to non-EU equipment. Moreover, the proposed European loan mechanism of €150 billion plans for targeted spending of at least 65% on European products.

It is also essential to finance the entire production chain because, while the main players have advance payments on the orders placed with them, this is not necessarily the case for medium-sized players who will have to face significant increases in their working capital requirements.

In the white paper on defense, Europe mentions as priority expenditures: air and missile defense, artillery systems, munitions, missiles, drones, and anti-drone systems. In the longer term, Europe's target is to strengthen its security and prepare to defend itself without relying on U.S. assistance.

The portfolio manager's view

Defense-related stocks outperformed the entire European market in 2024, and this trend continued into early 2025 in a context of substantial increases in military spending and a possible disengagement of the United States regarding the defense of the European Union. The new defense spending targets for 2030 provide some visibility on the medium-term prospects of the sector.

While the European and German plans have just been announced, there are still many unknowns regarding the nature and timing of the expenditures that will be incurred. Moreover, most companies in the sector have not yet communicated on the impact of these plans on their growth prospects, as seen with Rheinmetall, which is counting on its investor day scheduled for the second half of the year to unveil its new 2030 objectives. Nevertheless, it seems relevant to prioritize sectors where under-investment is most glaring, such as land equipment and munitions, as well as German stocks, since the country's budgetary leeway should allow for a faster ramp-up of investments.

The European defense sector is characterized by low standardization of weapon systems due to the fragmentation of players. For example, Europe has 23 times more types of land equipment than the United States, three times more types of aerospace equipment, and six times more types of naval equipment, which is economically less efficient and militarily less effective. To accelerate a standardization that seems inevitable, several European players are forming joint ventures to share technologies and increase economies of scale.

Thus, the German player Rheinmetall and the Italian player Leonardo have launched their joint venture for tank construction. The two partners will each hold 50% of this new entity to meet the Italian government's demand for an order of armored vehicles, a contract worth between €20 billion and €25 billion. Rheinmetall's "Panther" battle tank and "Lynx" infantry fighting vehicle will serve as the basis. Furthermore, this joint venture will also serve as an export base for other partner countries. Finally, Rheinmetall's CEO, Armin Papperger, views this joint venture as a first step towards consolidating the sector.

It is also worth noting that European states have repeatedly encouraged cooperation among a few major groups for large-scale projects, such as the Eurofighter Typhoon (BAE Systems, Leonardo, Airbus), the Future Combat Air System (SCAF) with Airbus, Dassault Aviation, and Indra as industrial coordinators, as well as European companies that are subsidiaries of several major groups like MBDA, a subsidiary of Airbus, BAE Systems, and Leonardo.

In light of the competitiveness challenges in the sector and the increased interoperability of European equipment, it is likely that these trends will strengthen in the coming years.

At CPRAM, the theme of European Strategic Autonomy allows exposure to the dynamics of the defense sector, as this theme appears to be an essential dimension of European strategic autonomy.