European strategic autonomy depends on the energy transition

Even before the outbreak of the war in Iran, the issue of energy costs and the competitiveness of European industry was at the heart of the European Commission’s discussions. Recent events have only reinforced the urgency of making progress on these issues, and the discussions of the European Council on 19–20 March have provided some guidance for the coming months.

Published on 13 April 2026

One Europe, one market

Presented as an action plan for 2027 to strengthen European strategic autonomy and resilience, it aims both to deepen the single market and to simplify administrative procedures for businesses and individuals. Among the concrete measures envisaged is the creation of a 28th regime for European companies, which would allow them to carry out their activities in all Member States, following the model of the unitary patent. Electronic reporting for cross-border services and a digital identity for businesses are also being advanced. Finally, competition rules could be reviewed to encourage the emergence of European champions..

On the simplification side, the Council asks European legislators to give priority, wherever possible, to regulations over directives, which would avoid lengthy and not necessarily uniform transpositions across countries. In addition, following the simplification texts on environmental regulations, a new omnibus simplification package on AI1 is planned by July 2026.

A reform but not a suspension of the carbon market

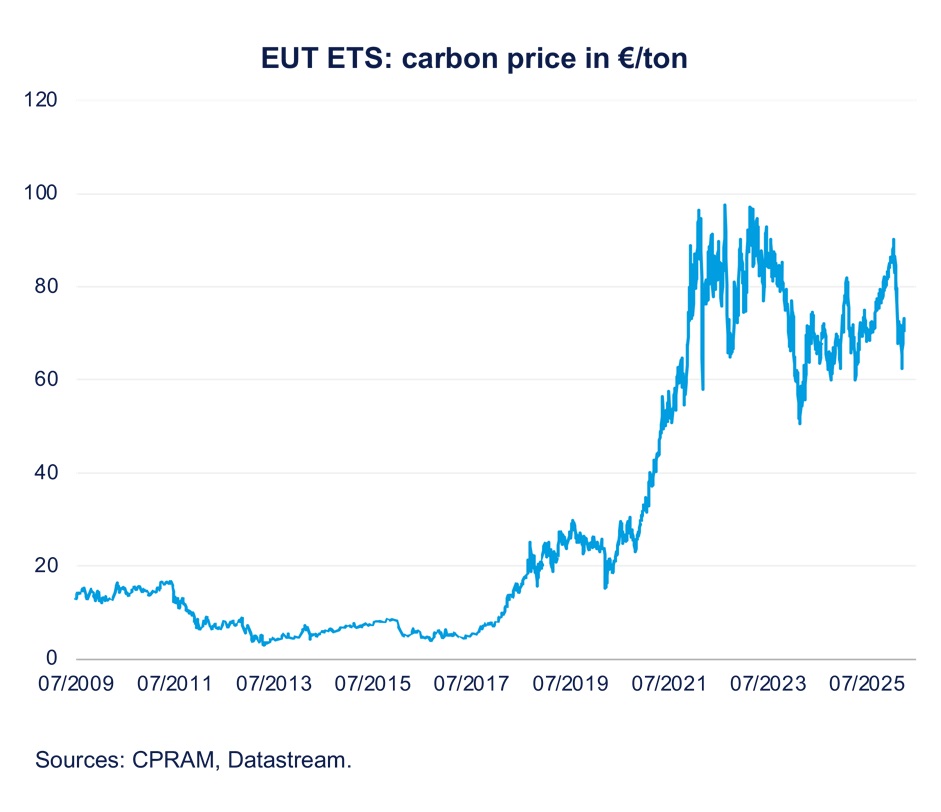

The acceleration of the path to reducing CO2 emissions decided for the European Union over the coming years is accompanied by a reduction in the greenhouse gas emissions cap for companies (-62% between 2005 and 2030 for companies subject to the European carbon market). This has led to a sharp increase in the price of carbon allowances, which ranged between €80 and €100 per ton at the end of 2025 and the beginning of 2026.

In addition, free allowances allocated to some industrial sectors are to be phased out between 2026 and 2034, as the carbon border adjustment mechanism (CBAM2) comes into force.

In July 2025, ten countries, including France, had asked for adjustments to the European carbon market for energy- intensive industries. More recently, a joint declaration by 13 countries stressed that “decarbonization must not be achieved at the cost of deindustrialization” and called for a reform of the market. However, positions on the desired level of reform remain far from aligned. Following the outbreak of the war in Iran, Italy went further and called for the suspension of the carbon market.

At the European Council on 19–20 March, European governments formally requested that the European Commission propose reforms to the European carbon market by next July, “in order to reduce carbon price volatility and mitigate its impact on electricity prices.”

The Commission recently rejected requests to suspend carbon tax for fertilizer producers, on the grounds that the ETS3 mechanism should remain predictable for producers. However, it announced at the end of March that it would review the market stability reserve mechanism, which aims to reduce carbon price volatility (by setting aside unsold allowances during the year, with a cap on the overall size of the reserve). A more comprehensive reform is planned for the summer and should focus on the timing of the end of free allowance allocations, the market stability reserve, and sectoral extensions (transport and buildings in ETS3). This second carbon market, whose implementation had already been postponed from 2027 to 2028, could be delayed again.

European carbon allowance prices have moved in line with reform announcements: they reached a low of €62 per ton on 19 March, at the height of the criticism of the European mechanism, then rebounded after the European Council to rise back above €70 per ton.

The energy transition is the most effective strategy for the EU's strategic autonomy

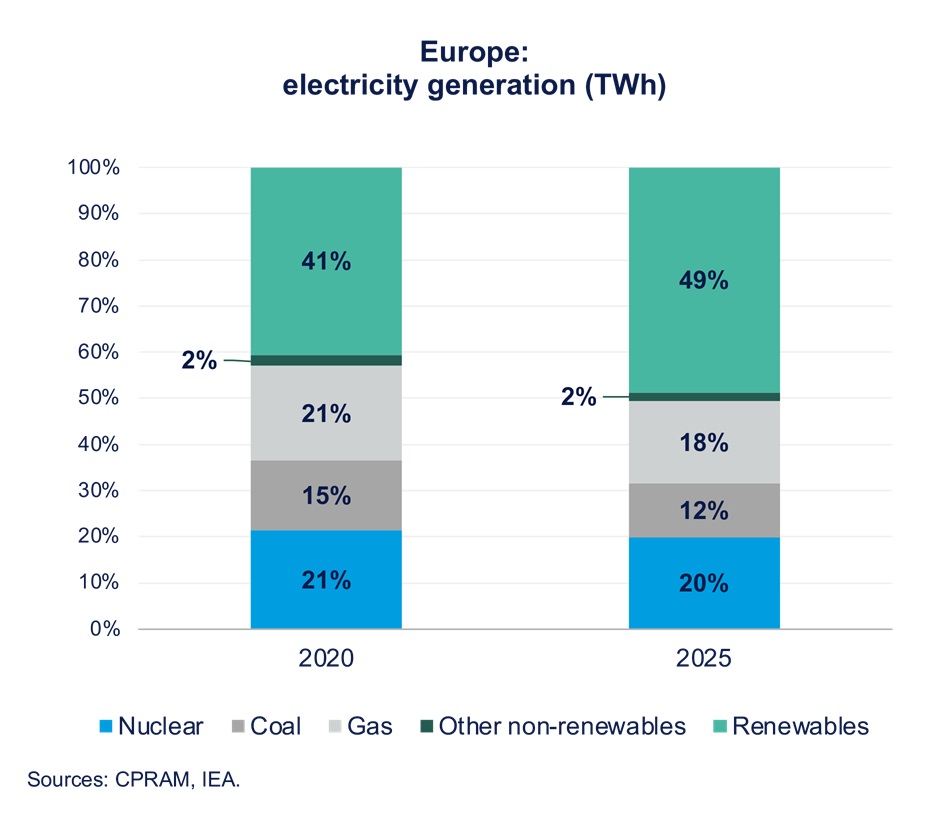

The Council recalled that accelerating the deployment of low-emission energy sources and developing storage capacities are the most effective structural responses to Europe’s dependence on energy imports. The euro area’s energy deficit reached €265 billion in 2025, but the 2022 crisis caused a surge in the energy deficit, which peaked at nearly €600 billion. Since 2020, the European Union has significantly increased the share of renewable energy in its electricity mix, from 43% to nearly 51% in 2025. It has also completely changed its approach to nuclear power, which now appears to be a technology to be developed.

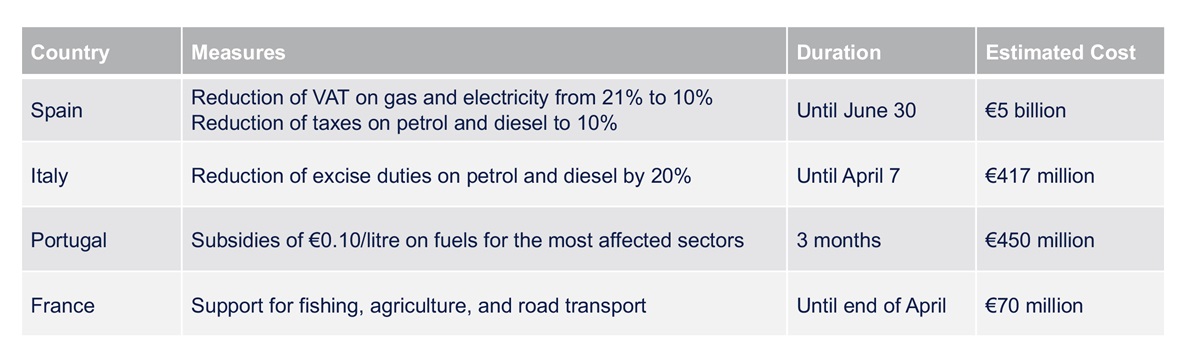

In the short term, the sharp rise in energy prices calls for a response, but unlike the “whatever it takes” approach adopted in 2020–2022, the government measures taken by the various Member States have been much more targeted and limited in size. Only Spain, which has slightly greater fiscal room than its neighbours, has departed from this moderation by announcing tax cuts worth nearly €5 billion. Europe is also proposing coordinated LNG4 purchases ahead of winter with the main international buyers, Japan and Korea.

Limited support measures

The 2022 crisis has led to structural changes in Europe, particularly in energy and defence policy, and the current crisis reinforces the investment choices already made and the need to go further. The issue of the competitiveness of European industry, highlighted by the Draghi report, is the subject of broad consensus, but progress on this front is more complex to achieve and should remain on the European agenda for the long term.

1. AI: Artificial Intelligence.

2. European dispositif CBAM: Carbon Border Adjustment Mechanism

3. ETS: Emissions Trading System, système.

4. LNG: Liquefied Natural Gas