Why Generative Artificial Intelligence is Redrawing the Map of Technology?

Published on 11 May 2026

Tech: The Historic Break between Manufacturers and Publishers

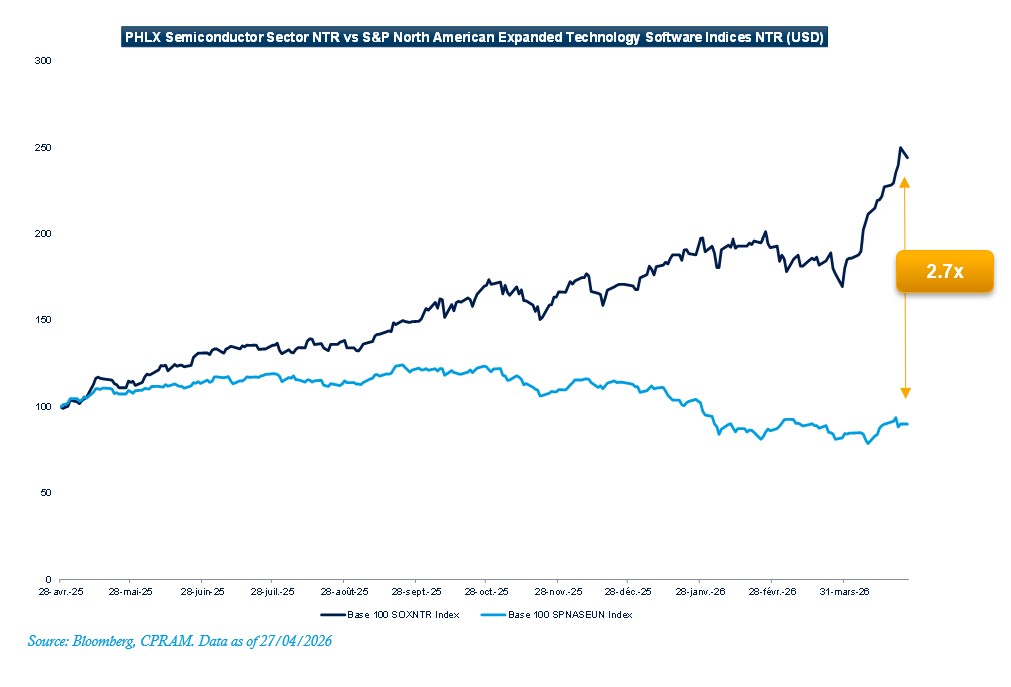

For the past 18 months, the global technology industry has been marked by a spectacular dispersion of performance between its two flagship sectors: semiconductors and software (also known as "SaaS" for "Software-as-a-Service"). To illustrate this phenomenon, we compared the SOX (PHLX Semiconductor Sector Index), which includes the world's main semiconductor players (Nvidia, Broadcom, ASML, etc.), to the SPNAS (S&P North American Expanded Technology Software Index), which is representative of software companies listed in the United States.

Over one year, the SOX index recorded an impressive increase of +144% (+45% since the beginning of the year), driven by the explosion in demand for Artificial Intelligence ("AI") and the acceleration of investments in digital infrastructure. Conversely, the SPNAS index experienced its strongest non-recessionary drawdown in more than 25 years, with a -10% decline over one year (-19% since the beginning of the year), reflecting a real mistrust of investors towards the traditional SaaS model.

This historical divergence between the two segments reflects a massive reallocation of flows within Tech: investors continue to favour AI "Picks and Shovels" (semiconductors, infrastructure) to the detriment of software publishers, whose ability to defend their position in the value chain is increasingly questioned in the era of generative AI.

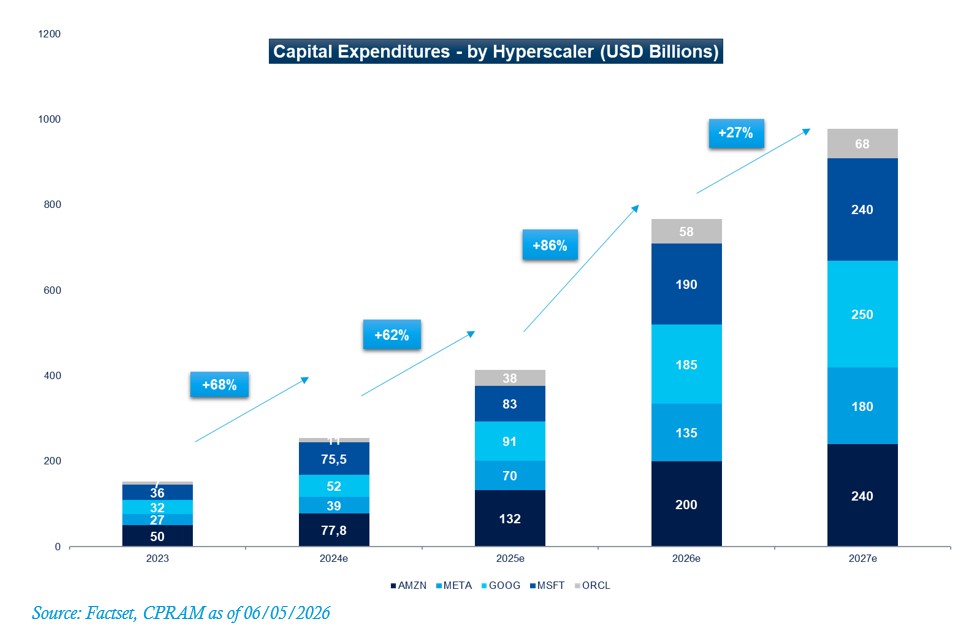

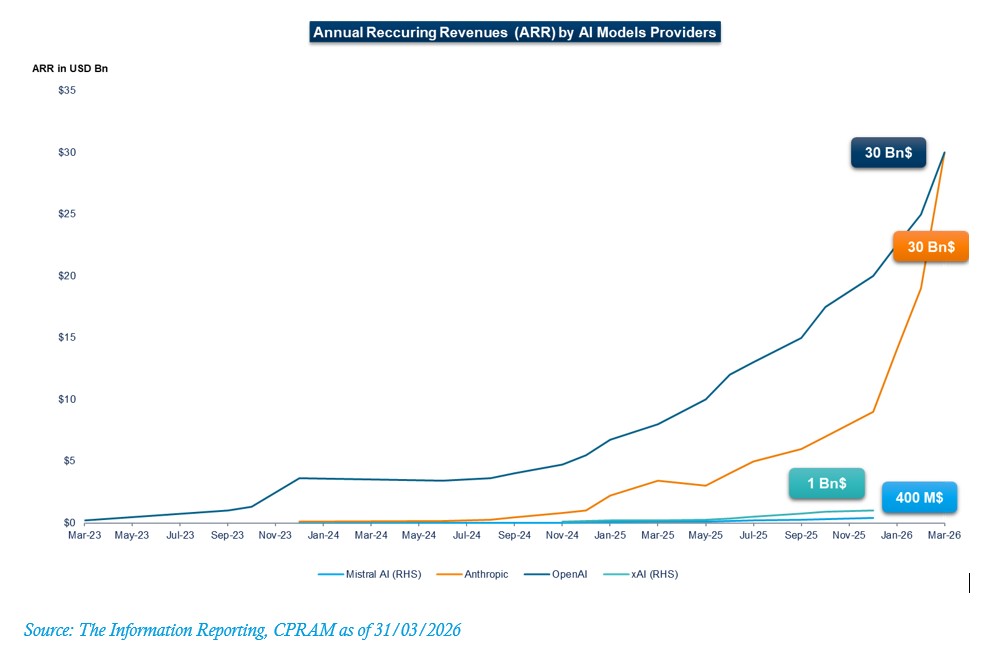

The clearest signal supporting this trade-off comes from hyperscaler1 investment: capital expenditure expectations for 2026 were revised from around $525 billion to nearly $750 billion after the latest Q1 26 quarterly releases. Unlike the cycle of the late 1990s, it is not a question of building in the hope of future demand: demand is already observable and the constraint now relates to available capacity. It is manifested in the acceleration of cloud revenues among all American players, in the increase in computing volumes (tokens) and in ambitious expansion plans. Amazon, for example, is talking about doubling capacity by 2028. At the same time, monetization is accelerating: the annualized revenue of major model providers has doubled in six months, with OpenAI and Anthropic approaching $60 billion between them. Anthropic's growth, with $21 billion in additional annual recurring revenue in three months, reinforces this diagnosis: value creation is primarily focused on the infrastructure/model provider, while software valuations are more likely to include the risk of competitive destabilization.

AI Labs: The Announcements that Shake the Stock Market

Regular announcements from major AI labs, such as OpenAI or Anthropic, have provoked often disproportionate market reactions. A simple press release or a technological demonstration can lead to significant price movements, including on companies that are not directly affected. This nervousness creates opportunities for disciplined investors, who are able to distinguish between media noise and real structural change.

We have seen this recently with striking examples such as CrowdStrike and Booking.com, where a single announcement from artificial intelligence labs (“AI Labs”) triggered significant share price swings within just a few hours.

For instance, in February 2026, Anthropic announced the launch of “Claude Code Security,” a new feature integrated into Claude Code, available in limited access for enterprises and teams. This technology automatically scans codebases for security vulnerabilities and suggests targeted patches for human expert validation. Anthropic highlights Claude’s ability to detect novel and complex flaws, often invisible to traditional tools, and to accelerate the remediation of vulnerabilities in a context of cybersecurity talent shortages. The announcement immediately raised concerns about the potential rapid disintermediation of established cybersecurity players such as CrowdStrike, leading to sharp volatility in the stock, even though this is not part of CrowdStrike’s core value proposition, and Anthropic’s solution is still only in a testing and co-development phase with clients.

In the travel sector, OpenAI recently acknowledged that, despite integrating search and booking features into ChatGPT, most users still prefer to finalize their reservations directly on the provider’s website, such as Booking.com, rather than completing the transaction within the ChatGPT interface. In response, OpenAI announced the development of a dedicated travel platform, thus shifting from the role of a mere disruptor to that of a direct competitor to traditional players. This strategic clarification led to a sharp appreciation in Booking.com’s share price, as investors now anticipate direct competition rather than just a threat of disintermediation.

This volatility is also explained by the intense media activity of the AI Labs, which skilfully orchestrate their communications to expand their addressable market and support their valuations ahead of IPOs. Initially concentrated in the software sector, these excessive reactions quickly spread to other industries, notably e-commerce, travel booking, online advertising, education, and financial services, where concerns about AI-driven disruption have also triggered marked market movements.

Yet not all promises of disintermediation materialize: strategies evolve, and many of the feared scenarios will not come to pass.

Software: What are the New Growth Drivers? What are the Risks?

Marked Dispersion within the Software itself

Behind this correction, however, there are significant disparities between segments.

In order to highlight them, we have reclassified each security in our funds into four distinct segments: Horizontal Software, Vertical, Cybersecurity and Other, isolating the specific case of Microsoft.

It is essential to define each segment well to understand the current dynamics:

- Horizontal Software: Generic solutions used in most industries (e.g., Salesforce, ServiceNow, Workday, SAP ). Their value lies in the standardization of key functions (CRM, HR, project management).

- Vertical software: Industry-specific solutions (e.g., Procore for construction, Veeva for healthcare, Guidewire for insurance ).

- Cybersecurity: Data and infrastructure protection software (e.g., Palo Alto Networks, Crowdstrike, Fortinet ). This segment is benefiting from structural demand, reinforced by the increasing sophistication of threats and the adoption of AI.

- A special case of Microsoft: Microsoft occupies a truly hybrid position in the software world. The company is both the world leader in horizontal suites (with Office, Dynamics) and a key player in cloud infrastructure (Azure), while integrating artificial intelligence into all of its offerings (Copilot, Azure AI). Its extraordinary size, with a market capitalization of more than $3,850 billion2 (nearly a third of the total capitalization of the global software sector), its deep integration with customers, the richness of its ecosystem and its capacity for continuous innovation make it a unique player.

For this reason, in our sub-segment performance analysis, we explicitly distinguish between non-Microsoft horizontal software.

This approach better reflects the reality of other players in the sector, without Microsoft's exceptional weight masking trends specific to horizontal and vertical software or cybersecurity.

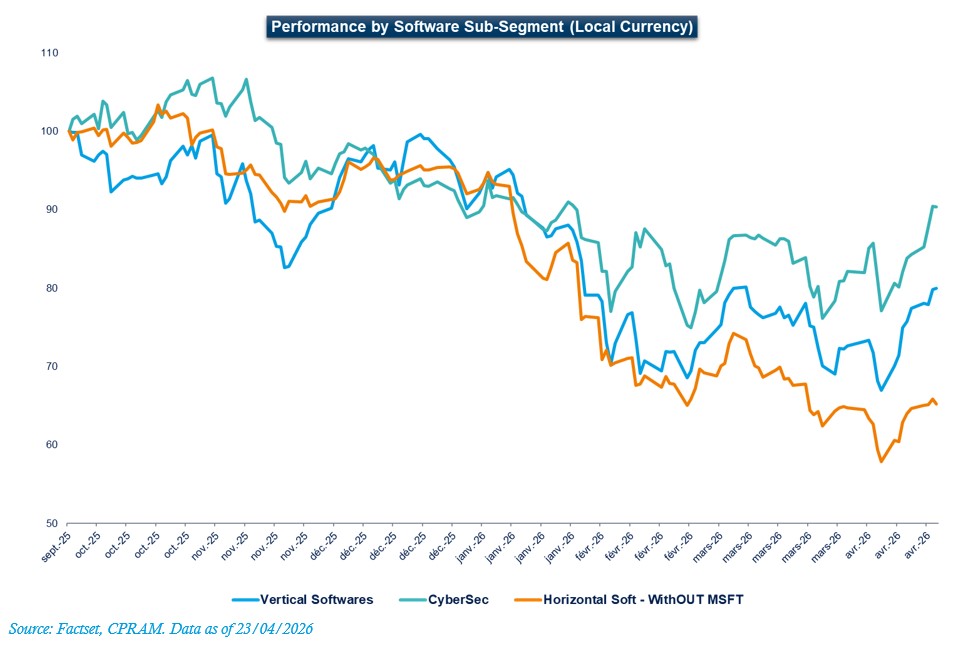

Within the sector, discrimination was very clearly reflected in stock market performance: cybersecurity only corrected about 10%, vertical software nearly 20%, while horizontal software lost about 35% since September 2025. This dispersion does not reflect a simple sector rotation, but a reassessment of the degree of substitutability and resilience of each sub-segment. Cybersecurity retains a more defensive profile, supported by structural demand, non-negotiable security requirements, and high replacement costs. Vertical softwares is more resilient than generalist solutions thanks to its deep integration into business processes and regulatory barriers. Conversely, horizontal softwares appears to be more exposed, because its standardized functionalities are more easily challenged by competition, by pressure on prices, and now by the rise of AI and low-code, which accelerate the commoditization of part of their offer.

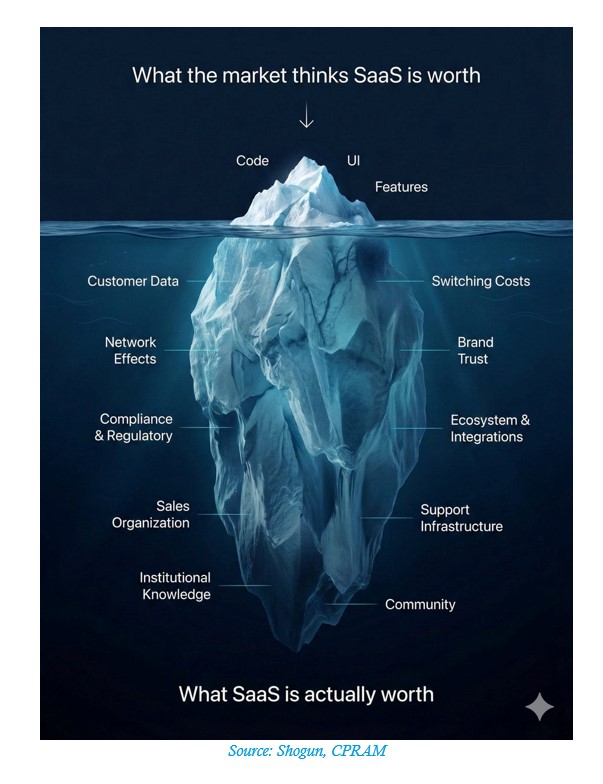

The Invisible that Matters: Why not all SaaS is Created Equal

The value of software is not limited to its interface or visible features. It's the depth of data, integration into business processes, and the ability to meet critical needs that make up the true competitive advantage.

The most resilient solutions are those that are deeply rooted in their customers' organizations and difficult to replace.

The New Drivers of Growth and Valuation

We consider that mission-critical software (ERP, cybersecurity, databases, verticals) remains the best positioned to benefit from a positive reassessment, thanks to:

- Ability to integrate AI to strengthen the offer: Players able to enrich their solutions with proprietary AI features (advanced automation, business co-pilots, predictive analytics) can increase their added value, build customer loyalty and justify a price upgrade.

- Platform and ecosystem effect: Publishers who manage to federate an ecosystem of partners, APIs and add-ons (e.g. Microsoft) benefit from a network effect that strengthens their "moat"3 and their negotiating power.

- Data monetization: Software that exploits large volumes of proprietary data (ERP, verticals, cybersecurity) can generate new growth drivers through the valorization of this data (insights, sector benchmarks, personalized services).

- Sector consolidation: The correction in valuations is paving the way for M&A transactions, allowing leaders to strengthen their position, accelerate innovation and capture market share at a lower cost.

- Regulation and compliance: Solutions capable of supporting customers in the management of regulatory compliance (GDPR, security, traceability) are becoming essential, which secures their installed base and their pricing power.

- Improved operating profitability: Increased cost discipline (including the reduction in share/SBC compensation) and the ability to generate free cash flow4 provide rerating leverage if growth picks up.

- Strategic repositioning: Some players, thanks to their agility, can pivot to new markets or business models (e.g. moving from "per capita" billing to value-based or usage-based billing), which can revive the growth dynamic.

In summary, the ability to innovate, monetize AI, exploit data and adapt quickly to changing customer needs is the basis of the opportunities for the best positioned players.

Beware of the Fall: The Risks Facing SaaS

Conversely, several structural risks weigh on the terminal value of SaaS players:

- Deflation of revenue per user: AI makes it possible to do more with less, which threatens "per seat" pricing models (e.g. Adobe, -30% YTD5 , victim of the fear of a massive reduction in licenses sold).

- Disintermediation by AI models: "Vibe coding" and "Do it Yourself" solutions could marginalize the least differentiated applications (e.g. Salesforce, -31% YTD6 , under the threat of hyperscalers).

- Dilution risk: An SBC that is too high continues to weigh on financial performance and investor confidence.

- Reallocation of IT budgets: Customers are increasingly choosing between legacy solutions and new AI tools, which can delay the resumption of growth.

- Decline in valuation multiples: Any questioning of the ability to generate growth or justify current multiples can lead to a lasting contraction in the terminal value.

We are not witnessing a generalized bankruptcy of the sector, but a period of questioning the criticality of each software layer, and a shift of added value within the software chain.

In summary, the combination of structural pressures on business models, risks of technological substitution and uncertainties about the ability to sustain growth makes selective and prudent management in the SaaS sector essential.

1 - A hyperscaler is a major cloud service provider capable of offering compute and storage services at scale. There is no official or consensus standard defining when to talk about hyperscalers, but giants such as Amazon Web Services, Google Cloud, Microsoft Azure, IBM Cloud and Alibaba Cloud are among them.

2 - Source: Bloomberg, CPRAM as of 28/04/2026

3 - The "moat", which can be economically translated as "sustainable competitive advantage", is a concept popularized by investor Warren Buffett. It represents a company's ability to maintain a sustainable competitive advantage over its rivals over the long term.

4 - Free cash flow is a company's ability to generate additional resources.

5 - Source: Bloomberg, CPRAM as of 28/04/2026

6 - Source: Bloomberg, CPRAM as of 28/04/2026

Disclaimer :

Past performance is not a guarantee of, and should not be considered an indicator of, future performance. The comments, estimates, views, analyses and projections regarding markets and their developments reflect CPRAM’s opinion as of the publication date and do not engage the company’s responsibility. The information provided has no contractual value and does not constitute investment advice or a recommendation to buy or sell.

This document is based on sources that CPRAM considers reliable at the time of publication.