Markets and strategies

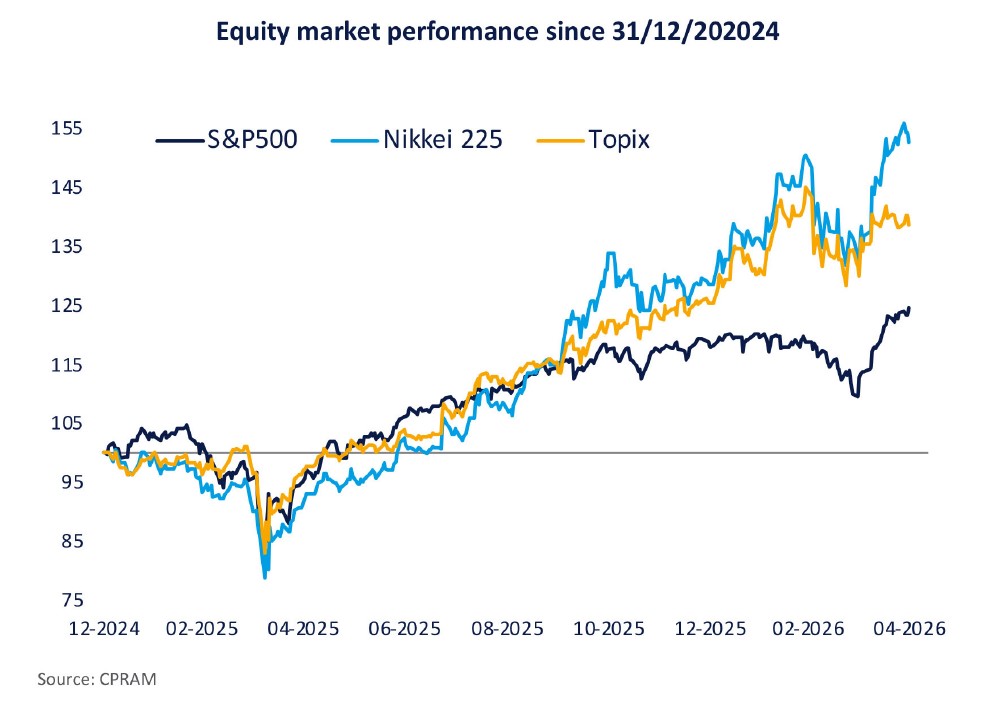

Japan, a very uneven rebound…

Since 7 April and the announcement of the truce in the Middle East conflict, a sharp rebound in risky assets has been observed. This move has mainly benefited Asian equity markets, which may seem counterintuitive given the high exposure of many Asian countries to the conflict, as they are heavily dependent on imports from the Gulf.

Published on 18 May 2026

At first glance, performance at the end of April therefore appears to signal a return to the trend that prevailed before the conflict. However, significant disparities can be observed, particularly those linked to the very clear dominance of the tech/ AI theme. The recent performance of the Japanese market is certainly the clearest illustration of this.

The recent rebound in the Japanese equity market is in fact misleading, as it has been driven almost exclusively by renewed investor interest in the AI theme. As a result, we have observed divergent trajectories between the Nikkei index, which is more concentrated and more exposed to technology stocks, and the broader, more diversified Topix over the recent period, with one of the largest performance gaps of the past 25 years, reaching as much as 15 percentage points in favour of the former.

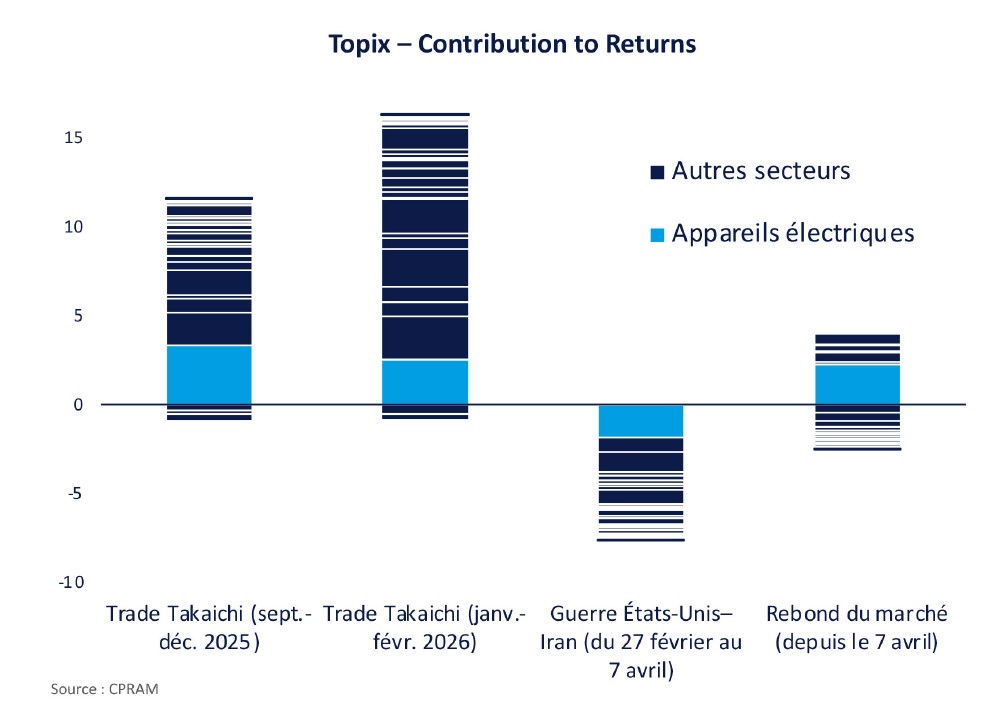

A more detailed analysis of Topix performance confirms this view. Between 7 April and 30 April, 21 of the 33 sectors making up the index posted negative performance. Another observation is that the “tech” sector was by far the largest contributor to performance, marking a stark difference from the previous upward phases of the past few months, during which the sources of performance were more diversified and balanced.

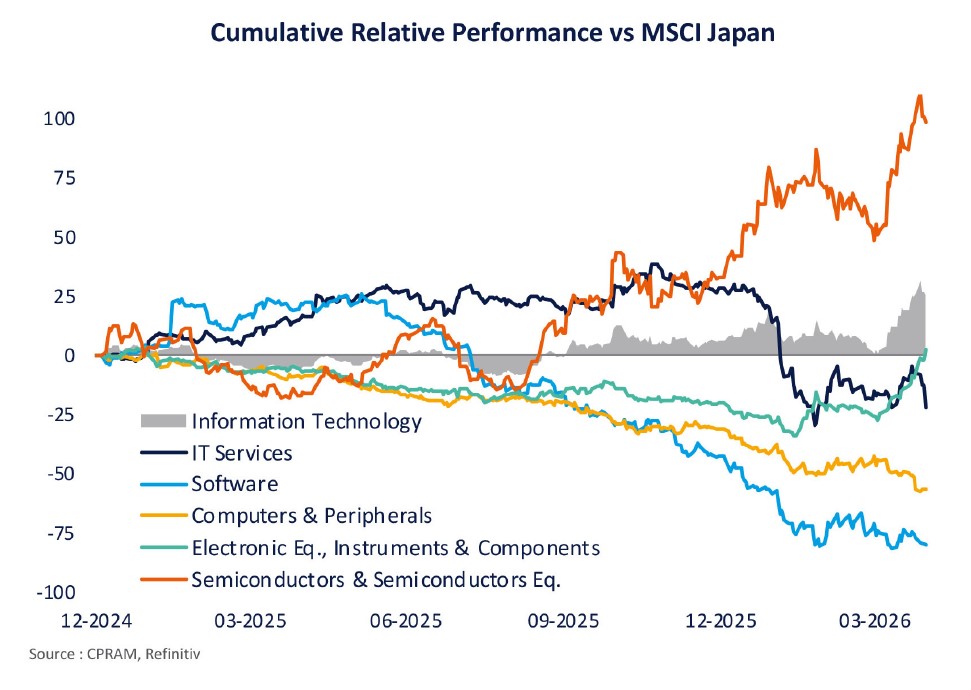

This does not, however, provide a faithful picture of the actual level of concentration, since within tech itself, the various sub-segments followed diametrically opposed paths. By the end of April, the “software and IT services” sub-sector of the MSCI Japan index had posted a sharp decline since the start of the year (-25.8%) and had extended its losses since 7 April. Equipment manufacturers and semiconductor makers, by contrast, recorded gains of +51.9% since the start of the year and a rebound of +26.4% since 7 April, respectively.

In the wake of this move, index concentration has mechanically increased. Within the Topix, the weight of the tech sector is back near its all-time highs and is close to 20%. Within the Nikkei, the stocks most inherently linked to the semiconductor cycle rank at the top: Advantest at 11.5%, Tokyo Electron at 7.5%, and SoftBank Group at 7.1%. While this remains far from extreme cases such as South Korea or Taiwan, it nonetheless must be acknowledged that the Japanese market has become more concentrated.

The recent rebound in the Japanese market is therefore not a resumption of the “Takaichi trade” that prevailed before the Middle East conflict, but rather part of a broader rebound in the AI cycle — more global geographically, but above all more targeted in sector and stock terms. Although the AI theme benefits from significant supportive factors, the strong concentration of performance is nevertheless a vulnerability for the Japanese market. All the more so because, outside of a scenario involving a lasting resolution to the conflict and the reopening of the Strait of Hormuz, it seems difficult to envision a catch-up move in the other sectors.

Informations :

Investing involves risks, including the risk of capital loss. Past performance is not a guarantee or indicator of future performance. Unless otherwise stated, all information contained in this document is sourced from CPR Asset Management and is accurate as of 07 May 2026.This communication is not contractual in nature but constitutes advertising communication. It is provided for informational purposes only and does not constitute a recommendation, analysis, or financial advice. Furthermore, it should not be considered as a solicitation, invitation, or offer to buy or sell collective investment schemes (CIS). Before subscribing to a collective investment scheme (CIS), the potential investor is advised to consult their advisor to ensure that the proposed investment is suitable for their financial and patrimonial situation. This document is based on sources that CPRAM considers reliable at the time of publication. Data, opinions, and analyses may be changed without notice. CPRAM disclaims any direct or indirect liability that may result from the use of the information contained in this document. CPRAM cannot be held responsible under any circumstances for any decision or investment made based on the information contained in this document. The information contained herein may not be copied, reproduced, modified, translated, or distributed without prior written authorization from CPRAM. All trademarks and logos used for illustrative purposes in this document are the property of their respective owners. This publication may not be reproduced, in whole or in part, or communicated to third parties without prior authorization from CPRAM. No guarantee is given that the market forecasts expressed in this document will materialize or that the trends referred to herein will continue. This publication is not intended for US persons as defined in the US Securities Act of 1933. MSCI information is exclusively intended for your internal use, may not be reproduced or redistributed in any form, and may not be used as a basis or component of any financial instrument, product, or index. None of the MSCI information is intended to constitute investment advice or a recommendation to take (or refrain from taking) any investment decision and may not be relied upon as such. Historical data and analyses should not be considered as an indication or guarantee of any analysis, forecast, or projection of future performance. MSCI information is provided "as is," and the use of this information implies assuming full risk related to any use of this information. MSCI, each of its affiliates, and other persons involved in compiling, calculating, or creating any MSCI information (collectively referred to as the "MSCI Parties"), or in connection with these activities, expressly disclaim any warranties (including, without limitation, any warranties of originality, accuracy, completeness, timeliness, non-infringement, merchantability, and fitness for a particular purpose) regarding this information. Without limiting the foregoing, under no circumstances shall any MSCI Party be liable for any direct, indirect, special, incidental, punitive, consequential damages (including, without limitation, loss of profits), or any other damages. (www.mscibarra.com). The information contained in this document belongs to Bloomberg and/or its content providers, may not be reproduced or redistributed, and offers no guarantee as to its accuracy, completeness, or relevance. Neither Bloomberg nor its content providers can be held responsible for any damages or losses resulting from the use of this information. All rights reserved. Refinitiv, all rights reserved. The information contained in this document is the property of Refinitiv and/or its content providers, may not be reproduced or redistributed, and is provided without any warranty as to its accuracy, completeness or suitability. Subject to compliance with its obligations, CPRAM cannot be held responsible for any financial or other consequences resulting from the investment. All regulatory documentation is available in French on the website www.cpram.com or upon simple request at the management company's headquarters. Nothing guarantees that the professionals currently employed by CPRAM will continue to be employed, nor that the past performance or successes of any of them will be indicative of their future performance or successes. For illustrative purposes only. CPR Asset Management, portfolio management company, authorized by the AMF under number GP 01-056 dated December 21, 2001 (Autorité des Marchés Financiers, 17 Place de la Bourse, 75082 Paris), public limited company with a capital of 61,461,945 euros, registered under number 399 392 141 RCS. 91-93 Boulevard Pasteur, 75730 Paris - Cedex 15 - France. Tel: +33 (0)1 53 15 70 00