China - A slow start for 2026

Published on 13 February 2026

The Chinese economy remains sluggish, and macroeconomic releases have been disappointing at the start of 2026. The weakness in activity is not a great surprise given that the real estate crisis is ongoing and continues to further erode the confidence of businesses but especially of Chinese households.

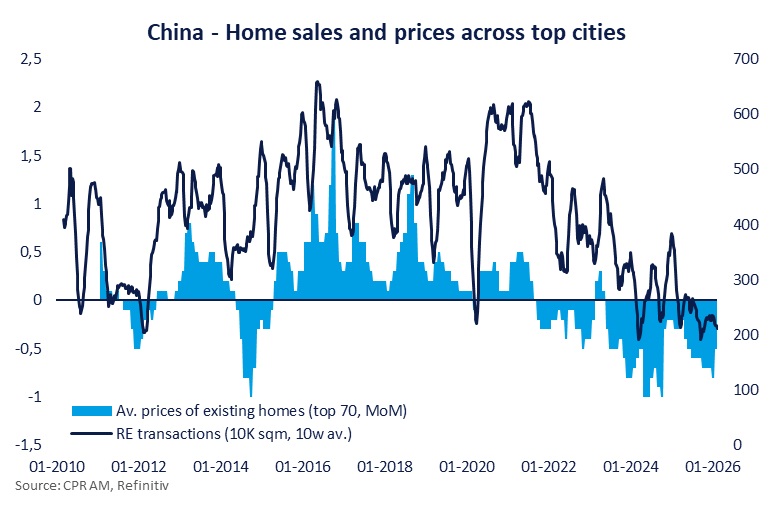

The real estate crisis continues without showing any real turnaround in January. The average prices observed in the 70 largest cities fell by -0.4% over the month for new properties (vs. -0.4% in December) and by -0.5% for existing homes (vs. -0.8%). The trend remains widespread across the entire territory: only 2 out of 70 provinces recorded price increases over the month for existing homes, and respectively 5 for new properties.

Some developers are calling for more measures from the authorities to curb the stock of available housing (close to historic highs) while sales continue to decline. According to S&P, the volume of real estate transactions is expected to continue to fall by 10 to 15% in 2026.

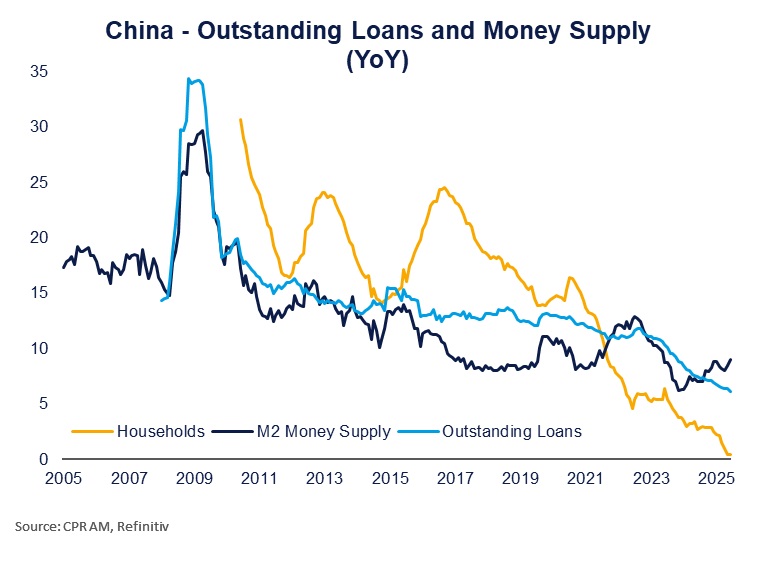

Bank credit demand remains very weak. The social financing of the economy overall came in line at 7 trillion RMB in January, but the momentum of public debt issuance masks the weakness of bank credit—which remains clearly visible in this release. Over the month, the total of new bank loans stood at 4.7 trillion versus 5 trillion expected. This figure is below those of January in the past three years, a sign that demand remains at a standstill. The volume of bank loans granted to households has stagnated over one year—a first since the publication of this statistic. Medium- to long-term loans to companies, reflecting their appetite to invest, show only a relatively weak increase compared to historical levels.

The sharp deterioration in the economic situation in the second half of 2025 did not prompt Beijing to drastically strengthen its support for the economy. Beyond declarations of intent, few tangible measures have been deployed, and the Chinese economy remains plagued by structural weaknesses. On the eve of the Lunar New Year, it would be surprising if the disappointing figures from the start of this year changed the situation.