How have central banks reacted to the war in Iran?

Last week, several major central banks (notably the Fed, ECB, BoJ, and BoE) held their monetary policy committees in a context of a sharp increase in energy prices. We review here the main points of convergence and the specificities in their assessments of the situation and their reactions.

Published on 23 March 2026

Common points

- Unsurprisingly, central banks perceive the rise in energy prices as having a negative impact on growth and upward pressure on inflation. They also indicate that uncertainty is particularly high. For example, Jerome Powell, Chair of the Federal Reserve, repeatedly said "We just don’t know," and Christine Lagarde, President of the European Central Bank, stated that "the war in the Middle East has made the outlook significantly more uncertain." The BoJ and the Riksbank also consider it too early to form a clear view of the impact on activity and inflation.

- Central banks have not made any rate decisions for the moment and prefer to take time to observe the evolution of energy prices. Andrew Bailey, Governor of the BoE, summarizes their stance well: "I want to caution against any hasty conclusions regarding a possible interest rate hike... Today, we have sent a very clear message: the position to adopt is the status quo."

- Central banks are well aware that they do not set energy prices. As Andrew Bailey says, "monetary policy cannot reverse the shock on energy prices," but the BoE can "respond to the risk of a more persistent effect on inflation."

- Beyond energy prices, the question already concerns second-round effects, that is, increases in non-energy prices in response to the rise in energy prices. The term "second-round effects" appeared, for example, eight times during Christine Lagarde’s press conference. Again, all central banks indicate that the longer the conflict lasts, the greater the risk of second-round effects. In this context, the issue of inflation expectations will be key in the reaction function. Jerome Powell indicated that the Fed might not overreact if long-term inflation expectations remain well anchored, and Christine Lagarde referred to the situation as the "three times 2%" scenario: 2% inflation in the medium term, 2% medium-term inflation expectations, and 2% interest rates.

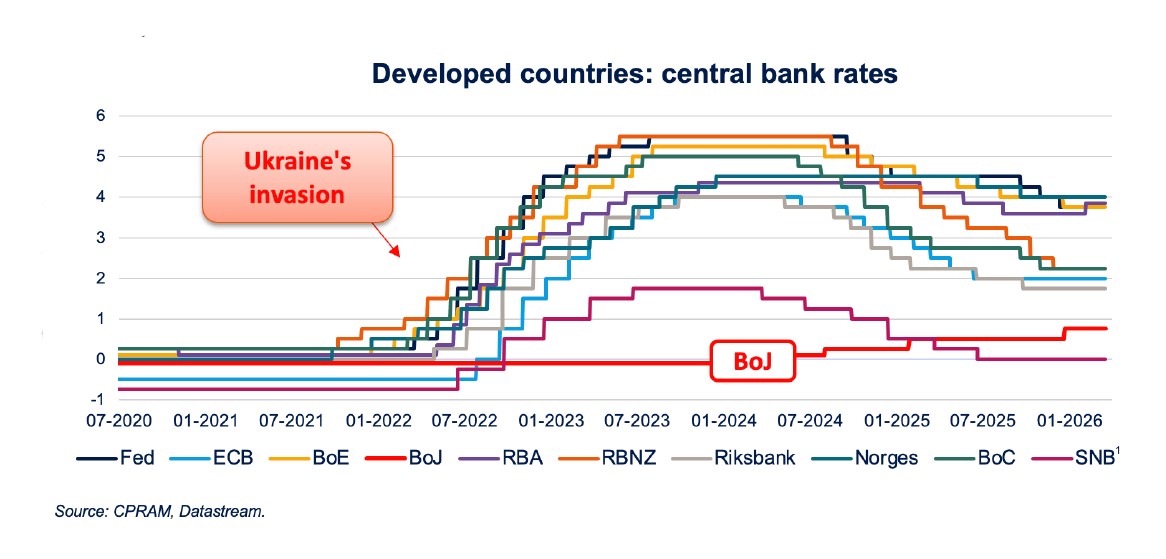

- Central banks indicate they are better positioned than during the 2022 energy crisis, mainly for two reasons: 1) policy rates are higher than in 2022 (at the beginning of 2022, no developed central bank had rates above 1%) and closer to neutral rates, 2) labor markets are significantly less tight than in 2022, which reduces the risk of second-round effects.

Country-specific details

- While most central banks have either lowered their growth forecasts or implied they might do so, the Fed raised its growth forecasts for 2026, 2027, 2028, and the long term. Jerome Powell explained that this was based on an assumption of stronger productivity growth. However, unemployment rate forecasts were barely changed (slightly raised for 2027). In reality, the Fed increasingly envisions a "jobless boom" scenario for the United States. FOMC members continue to show "dots" indicating rate cuts in 2026 and 2027, which would materialize if the expected disinflation occurs.

- Probably wary from the very high inflation of 2022 (peaking at 10.6%), the ECB has prepared "adverse" and "severe" scenarios for energy price developments. It is the only one to do so. This likely also reflects an awareness of Europe’s vulnerability regarding energy issues.

- The BoJ maintained a relatively hawkish communication and seems to seek to anchor expectations. However, its pause could be longer than expected due to high uncertainty.

- The RBA announced a second consecutive rate hike on March 17, and its governor expressed concern about possible second-round effects following energy price increases.

- The SNB implies it could intervene in the foreign exchange market to counter the appreciation of the Swiss franc, a traditional safe haven.

- The BoE and the Riksbank have maintained the possibility of rate cuts if the current shock proves short-lived.

- The Bank of Canada kept its key rate unchanged. But the situation is different for Canada because the Canadian economy can benefit from higher energy prices.

The energy price shock caused by the war in Iran will weigh on growth and push inflation higher, which is particularly uncomfortable for central banks. All emphasize the uncertainty related to the duration of the conflict and sought this week to buy time. The question already concerns possible second-round effects, but they generally indicate being better positioned than during the 2022 energy crisis, mainly for two reasons: 1) policy rates are higher than in 2022 and closer to neutral rates, 2) labor markets are significantly less tight than in 2022.

The portfolio manager's view

Following recent monetary policy committees, central bank communications were poorly received by the markets, which quickly and significantly revised their expectations for the year:

- Markets now anticipate a status quo for the Fed (whereas two rate cuts were expected at the end of February).

- For the ECB, expectations have shifted towards three rate hikes (compared to a half cut expected at the end of February).

- The Bank of England is now expected to raise rates by the equivalent of three and a half hikes (versus two cuts at the end of February).

This adjustment, as broad as it is rapid and modeled on the movements observed in 2022, seems premature to us as long as the persistence of energy price pressures for several months is not confirmed. We remain vigilant and are monitoring the evolution of economic and energy data to reassess our positioning.

Julien Daire, Deputy Director of Investments - CPRAM

Listed central banks: Fed (Federal Reserve, United States), ECB (European Central Bank, Eurozone), BoE (Bank of England, United Kingdom), BoJ (Bank of Japan, Japan), RBA (Reserve Bank of Australia, Australia), RBNZ (Reserve Bank of New Zealand, New Zealand), Riksbank (Sveriges Riksbank, Sweden), Norges (Norges Bank, Norway), BoC (Bank of Canada, Canada), SNB (Swiss National Bank, Switzerland).