Markets and strategies

Japan, the resounding comeback of the Yen

Published on 9 October 2024

What triggered the trend reversal in the yen?

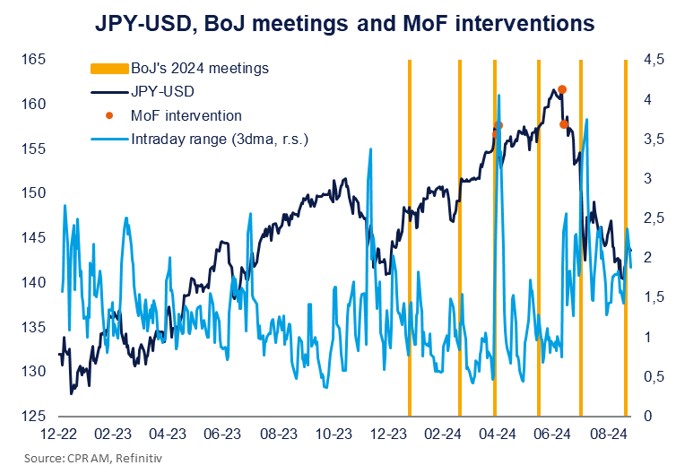

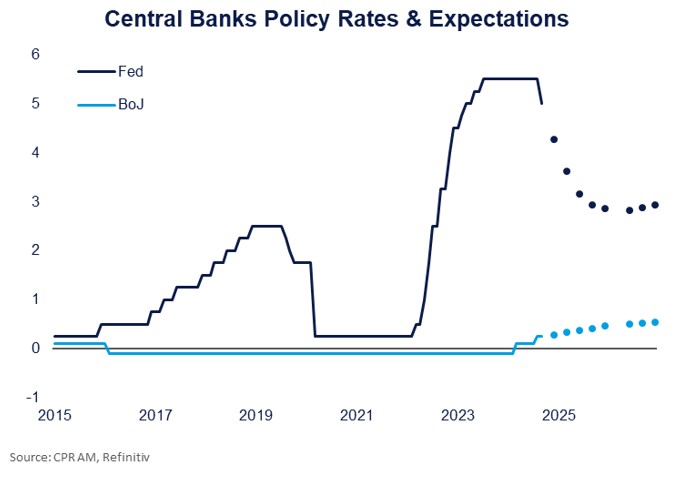

After ending its negative interest rate policy in March, the BoJ turned up the heat at its Monetary Policy Committee meeting at the end of July. Although the reduction in its asset purchase programme had largely been pre-announced, the central bank nevertheless created a surprise by simultaneously raising its main key rate to 0.25% at the end of July.

But it was above all Kazuo Ueda's hawkish turnaround that took investors by surprise, as they had previously been used to a very cautious stance from the BoJ governor. During the press conference, he clearly played down the impact of these rate hikes on the Japanese economy, while pledging to continue normalising monetary policy.

While the Ministry of Finance's intervention on the foreign exchange market (also a surprise) in mid-July had had only a moderate impact on the currency, this clear hardening of tone by the central bank anchored new expectations and triggered a rebound in the yen.

Worse still, the movement was subsequently fuelled by the publication of disappointing US figures (notably the July and August employment reports), arguing for a return to a phase of monetary easing on the other side of the Atlantic. While the BoJ's U-turn was certainly the trigger for the yen's rebound, tacit confirmation that the Fed would be cutting rates very soon also played a part.

How can we explain the speed, scale and repercussions of this movement?

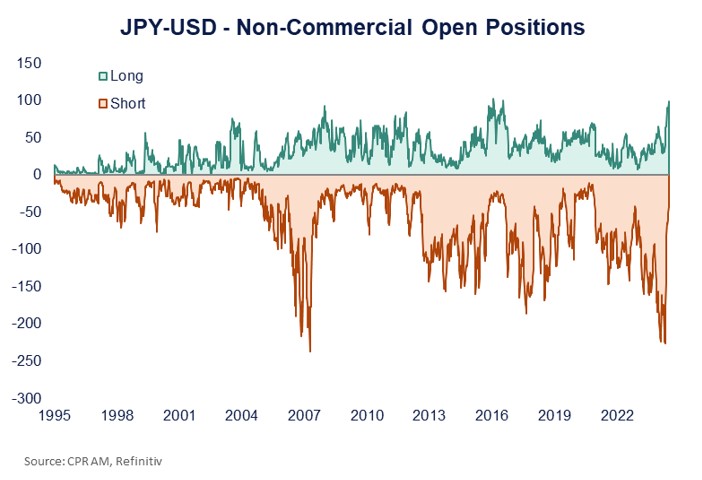

The suddenness of the yen's reappreciation can be explained in particular by the massive unwinding of short positions in the Japanese currency. Because of the yield differential between Japan and other economies, these positions had built up over the past 3 years to record levels. This positioning was not confined to hedge funds, but was widely accepted by asset managers and other institutional investors.

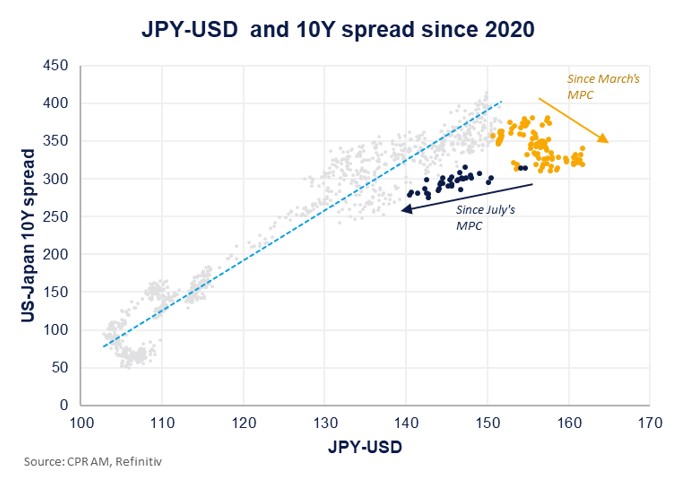

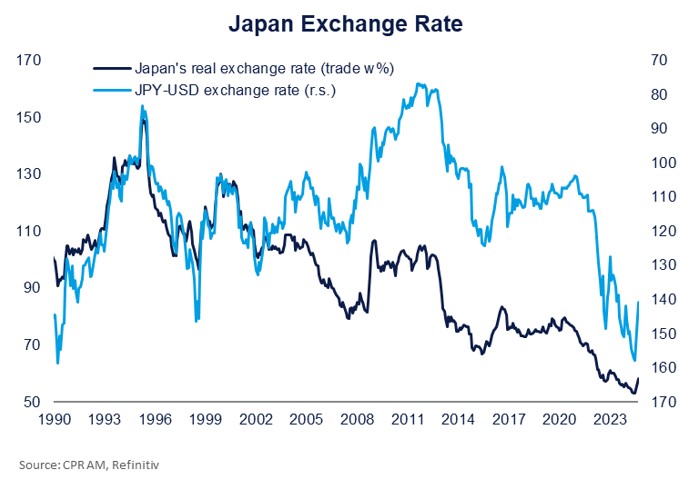

The magnitude of the movement is not so surprising, however, as it reflects a return to economic fundamentals. Since the start of the BoJ's normalisation phase last spring, the USDJPY exchange rate had in fact fallen out of step with the long-term interest rate differential between the United States and Japan, and this gap seems to have been rectified by the movement of the last few weeks, with the Japanese currency returning to levels close to those seen at the start of the year.

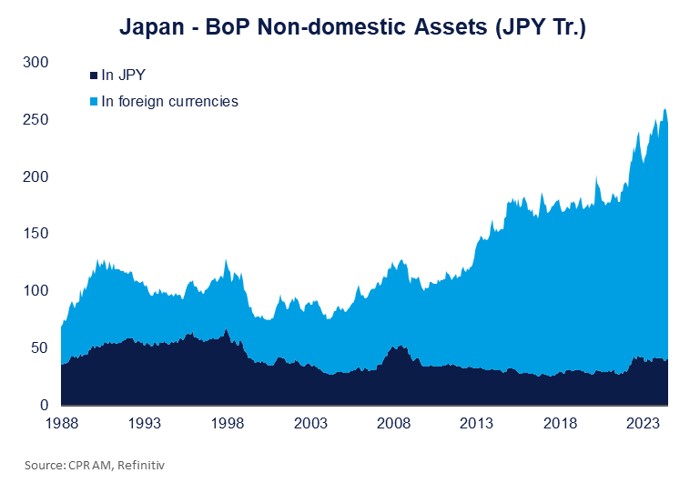

Beyond the appreciation of the yen, it was above all its repercussions on the financial sphere that came as a surprise. This contagion is linked to the fact that the Japanese currency has long been (and still is) used to finance so-called "carry trade" strategies, but also to the fact that the Japanese hold a considerable volume of foreign assets - investments doubly penalised by the appreciation of the yen and growing fears about US and global growth.

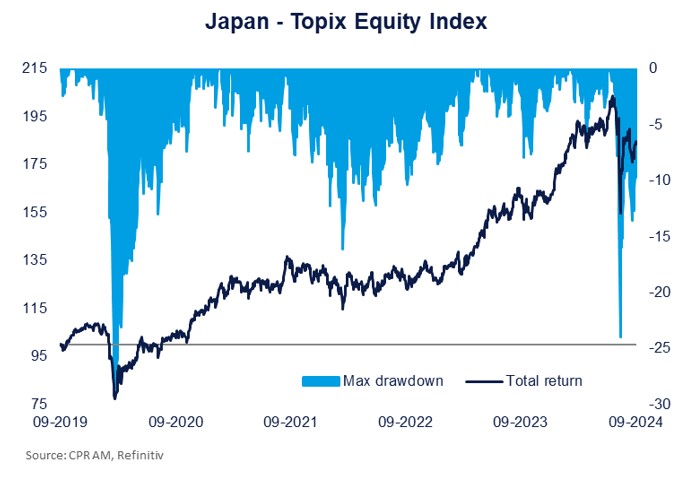

As a result, the shockwave spread mechanically to many asset classes, led by Japanese and US equities and momentum strategies. On 5 August, the Topix index recorded its worst session since 1973, falling by 12.2%, before partially erasing its losses over the following days. Some observers suggest that the recent fall in oil prices may have been accentuated by the continued appreciation of the yen and the unwinding of carry trade strategies.

Can the Japanese currency continue to appreciate?

Despite the fact that some of the ground already seems to have been covered, and that (relative) stabilisation is probably the most likely scenario in the short term, it is difficult to envisage any other path for the Japanese currency in the medium term, for a number of reasons.

Firstly, the recent improvement in economic figures suggests that the BoJ will continue to normalise its monetary policy. The viability of the recovery in demand will, of course, have to be confirmed over time, but the fall in imported inflation and the rise in wages - the cornerstone of the monetary authorities' scenario - point in this direction.

The BoJ's recent communication has been fairly consistent, with all its members adopting Kazuo Ueda's "hawkish" rhetoric at the July Monetary Policy Committee meeting: rates are currently very low; the economy is in line with the central bank's scenario; further rate hikes are to be expected. This new mantra was reaffirmed at the BoJ's September meeting, albeit with more dovish elements.

A few days earlier, the Fed had begun the process of recalibrating its monetary policy by announcing a 50bps cut. Jerome Powell's speech was not seen as particularly dovish, however, and gave no indication of the future path of Fed funds. But while the pace and magnitude of future rate cuts across the Atlantic remain uncertain, the yield differential between Japan and the United States should continue to narrow - and thus provide further support for the Japanese currency.

In addition, the normalisation of the BoJ's balance sheet policy should be accompanied by the return of banks to the JGB market. The reallocation of assets placed abroad to the domestic market will therefore be another argument in favour of a stronger yen. And while this movement will certainly be very gradual, the volumes are considerable and capital flows will continue to play a key role.

Finally, it should be stressed that despite the recent movement, the level of the yen (particularly in real terms) remains very low. Its medium- to long-term potential for appreciation therefore remains substantial.

Should we expect further volatility shocks?

An episode similar to that of early August seems unlikely in the short term. Other than stabilisation, the central scenario remains that the yen will continue to appreciate, but at a much more measured pace.

Investor positioning has rapidly normalised (particularly for speculative strategies), and has even reversed in the case of momentum/CTA players. Expectations now seem to be more in line with fundamentals, and this situation is likely to persist. In other words, "don't fight the BoJ" now seems a more credible mantra than it did a few weeks ago.

Moreover, various factors argue in favour of a pause on the part of the BoJ (electoral calendar, fall in first-order inflation, etc.). Over the recent period, several members have also stressed the need to take account of market instability in the conduct of monetary policy. At the September Monetary Policy Committee meeting, Kazuo Ueda made it clear that the central bank had room for manoeuvre in terms of timing ("We have some time to decide on policy").

In fact, while the episode at the beginning of August was the result of a combination of several concomitant factors, the 'gap' between Japanese and US monetary policies is likely to close more sequentially. While remaining dependent on Japanese figures, the BoJ will adjust its policy in line with the dynamics of the US economy (and therefore of the Fed), but also with market volatility.

That said, it seems difficult to rule out a continuation of the recent trend. A deterioration in US figures could prompt the Fed to step up its support for the economy, while an acceleration in the Japanese economy would force the BoJ to act, or risk losing credibility. Especially as the Japanese central bank's ability to surprise investors remains a major risk factor. The BoJ succeeded in balancing its rhetoric in September, but a possible return to a style of communication perceived as too hawkish could fuel volatility in the currency.

Summary

The BoJ's unexpected hawkish reversal and the deterioration in US figures led to a sharp rebound in the yen in early August.

This was followed by a massive unwinding of short positions in the Japanese currency and carry trade strategies, the shockwaves from which were mechanically passed on to a number of risky assets.

But despite the progress made, the Japanese currency remains weak by historical standards.

The yen is therefore likely to continue to strengthen in the medium term, not least because of the divergent paths taken by the BoJ (further normalisation) and the Fed (easing).

However, a repeat of August's volatility shock is unlikely in the short term, given the rapid adjustment in investor expectations and positioning, and the return to a more measured stance by Japan's central bank.