China: The response to the risk of deflation

Published on 12 November 2024

Some reminders about deflation?

Deflation is an economic phenomenon greatly feared by central banks, which can be defined as a decrease in the level of prices with three characteristics: 1) it is widespread, meaning it affects all prices, 2) it is persistent, lasting several years, and 3) it is anticipated by everyone (households, businesses, the state). This phenomenon is potentially very recessionary as rational agents postpone the purchase of goods and services or their investments if they anticipate that prices will decrease in the future.

As for the causes, economic theory generally holds that deflation can be caused by a negative shock to aggregate demand (bursting of a bubble, credit rationing, significant decrease in consumer confidence) or by a supply shock such as a sharp decrease in import prices.

Over the past decades, it is often noted that the risk of deflation has been high in Japan following the prolonged bursting of real estate and financial bubbles since the early 1990s (it took until 2024 for the Nikkei to reach its 1990 level!). Inflation in Japan averaged 0.1% over the period 1995-2020, and there were periods of negative inflation lasting several quarters. In response, the Bank of Japan implemented several operations, starting in 2001, and then in a much more dramatic manner under the presidency of Haruhiko Kuroda (2013-2023).

In the 2010s, the United States and Europe also faced the risk of deflation following the 2008 financial crisis. At the time, the housing crisis in the United States and in certain countries in the southern eurozone had significantly lowered real estate prices over time: by 26% between the peak of 2007 and the trough of 2012 in the United States, and by 41% between 2007 and 2015 in Spain. This had weighed on the inflation profile but had also led to a sharp increase in non-performing loans on bank balance sheets and a severe deterioration in the labor market. The prolonged weakening of demand, exacerbated in Europe by the sovereign debt crisis, had raised fears of a deflationary spiral.

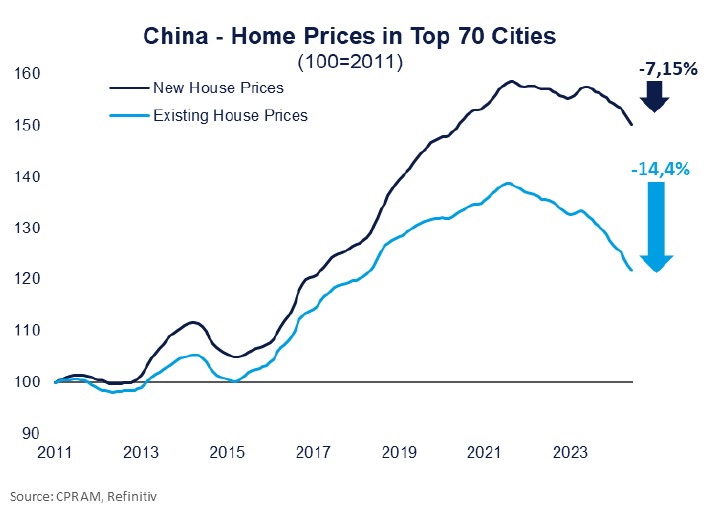

At the time, the fiscal response was measured in the United States due to the divided government and in Europe due to the promotion of fiscal consolidation as a remedy for the sovereign debt crisis. On the other hand, the monetary response was very powerful, with the implementation of unconventional policies such as forward guidance, significant quantitative easing operations, negative interest rates, and long-term refinancing operations. The significant decline in real estate prices and stock markets in China since 2021 has increased the risk of deflation.

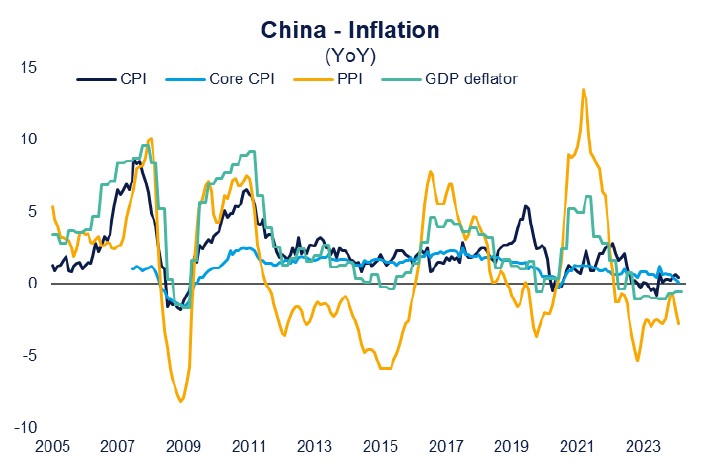

The evolution of underlying inflation, i.e., inflation excluding energy and food, clearly shows this: it has been trending downward for several years, reaching only +0.1% on a year-on-year basis in September 2024.

Proof that this issue is central is that the IMF published an estimate of a deflation vulnerability index for China last August. The conclusion of this work was that the current probability of deflation in China was still low, but the situation was such that further deterioration of fundamentals (i.e., widening of the output gap and continued decline in real estate and stock prices) could quickly increase this probability.

The Chinese authorities are obviously aware of the recent increase in deflation risks, which is why they have decided to react, as we will detail in the rest of this text.

Beijing awakens... after 3 (very) long years.

After a "false rebound" at the beginning of 2023, following the abandonment of the "zero covid" policy, the Chinese economy remains fragile as it is still plagued by a severe real estate crisis and debt issues.

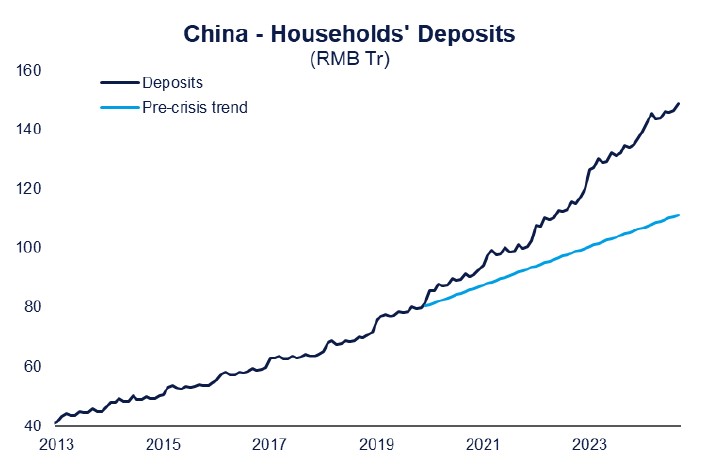

The responses from the Chinese authorities have been late, relatively timid, and scattered, resulting in a widespread loss of confidence. This has led to a vicious circle as this loss of confidence has itself led households to save more and consume less.

The gradual decline in interest rates and the easing of mortgage conditions have not overcome households' mistrust of the real estate market. This caution is also shared by banks, despite repeated calls from the government to facilitate their refinancing.

The eagerly welcomed real estate destocking plan in May has remained more or less at a standstill, while local governments continue to face debt issues compounded by declining revenues.

Another example: interventions by the "national team" (sovereign funds and large state-owned enterprises) aimed at supporting domestic stocks only took place in response to a sharp acceleration in market decline at the beginning of the year.

They only allowed for a very short-lived stabilization of the market, further eroding the already low confidence of households. Beyond the trajectory of prices and weak demand, it is especially the almost non-existent impact of traditionally adapted measures that raises concerns.

After more than 3 years of crisis and a public authority that has appeared, at best, "behind the curve," the specter of deflation has started to worry observers more and more.

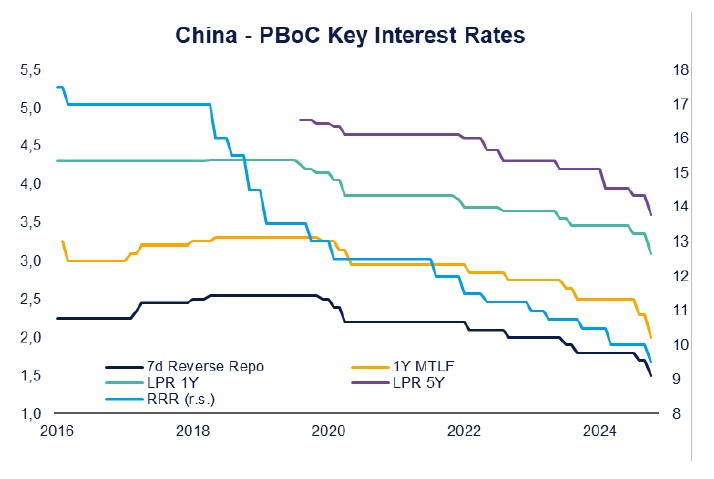

However, we undoubtedly witnessed in late September the awakening of the authorities, and it is through the PBoC that Beijing decided to send a strong message - which was greeted with a surge in the stock market.

While support measures were previously implemented sequentially, the central bank has made a clear break by announcing a range of measures covering a wide spectrum. This includes rate cuts (both effective and forthcoming), renegotiation of existing mortgage loans (saving households around 150 billion RMB), increased support for struggling developers (additional 2 trillion RMB), mechanisms facilitating share buybacks (at least 800 billion RMB), and a recapitalization plan for major commercial banks (1 trillion RMB).

The adjustment of certain pre-existing mechanisms is also commendable as it demonstrates a stronger commitment from the authorities: the PBoC now acts as a lender of last resort to revive the real estate destocking plan. This measure is expected to be complemented by a significant fiscal stimulus, the official announcement of which is expected after the next NPC meeting on November 8th.

While the details of this plan are yet to be specified, Reuters recently mentioned a multi-year program of 10 trillion RMB - approximately 8% of the current GDP - while also noting that this amount could be increased if necessary. This would therefore be the most significant measure since the 2008 crisis.

Beyond the announcements and the actual amounts, the real breakthrough lies in the coordinated aspect of public policies: Beijing no longer seems to provide isolated responses to specific shocks but is attempting to implement a comprehensive solution.

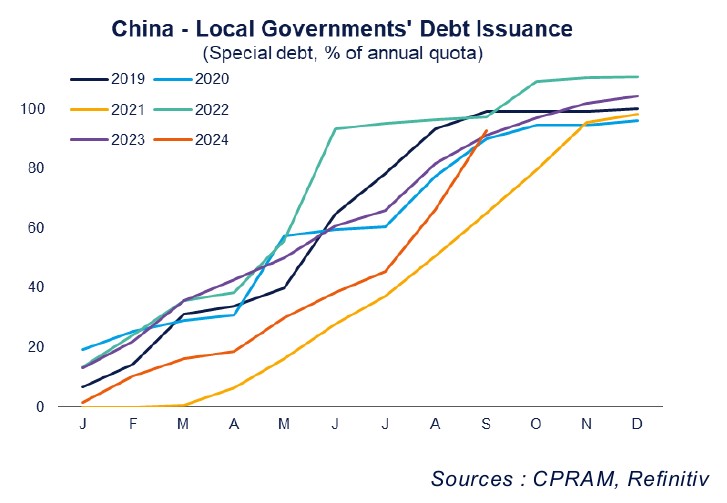

This positive signal has been reinforced by the reactivation of previously sluggish public entities (as evidenced by the significant increase in debt issuances), probably encouraged by the tougher tone and repeated encouragements from Xi Jinping. This should now ensure a better transmission of economic policy (particularly monetary policy).

However, some pieces still seem to be missing to complete this Chinese tangram.

The budget stimulus would thus mainly target the debt of local governments and the real estate sector. Unlike what was done during the 2008 crisis, the goal here is still to stabilize the economy by managing structural issues, rather than a policy of conjunctural demand stimulus. Direct support to Chinese households remains limited in the measures announced so far, which is unlikely to change for primarily ideological reasons. Xi's doctrine clearly warns against the dangers of "welfarism," while the concept of "common prosperity" refers more to inequality issues and would result in announcements such as support for precarious students (a beneficial measure, but with limited macroeconomic effects).

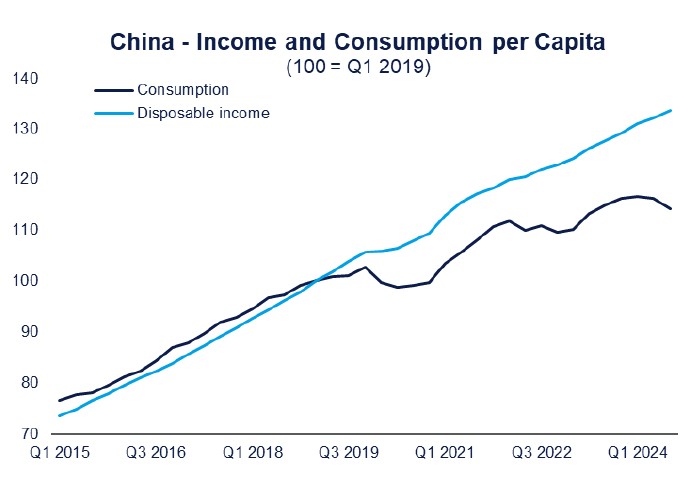

The stabilization of real estate prices, and to a lesser extent the rebound of the stock market, should certainly be perceived positively by households, but this may remain insufficient to sustainably restore their confidence in the future, especially in light of the ongoing deterioration of the labor market in recent years. The Chinese government must also provide responses to other key challenges, both conjunctural (geopolitical and trade tensions) and structural (population aging). In this regard, the recent awakening of the authorities to the risk of deflation sends a positive signal, but the current framework still appears incomplete in order to provide medium to long-term prospects.